Ag Markets May 11, 2020

Tomorrow we see the USDA's big May WASDE report and the first look at crop year 20/21 balance sheets.

Beyond Tuesday's fundamental trading inputs, agriculture traders have plenty of non-fundamental inputs to consider:

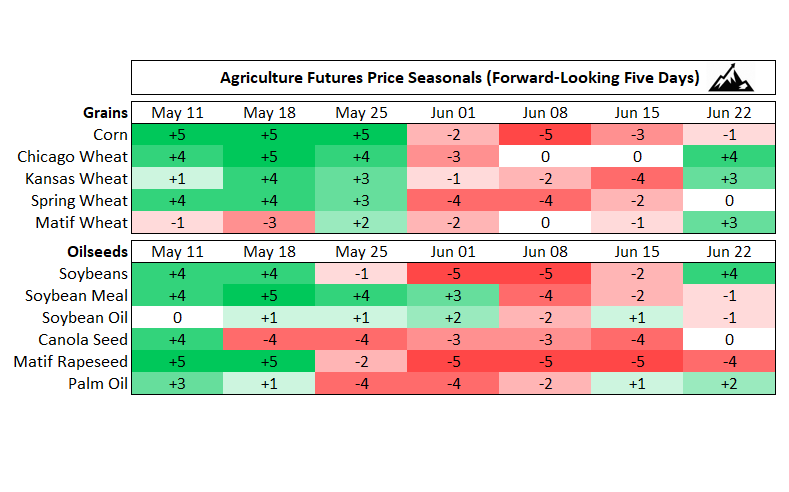

Price seasonals: We're in the most seasonally bullish weeks of the year for corn, chicago wheat, and soybean meal. Yesterday, May 10th, was the seasonal low for the ag complex last year, 2019, and our seasonal heat maps (chart of the week, below) are a sea of green for the coming weeks.

Macro: Friday's U.S. Nonfarm payrolls report showed a record -20.5 million jobs lost in April (largely priced in after April's miserable weekly jobless claim reports). This week we see U.S. retail sales, CPI inflation, Empire Manufacturing PMI, and jobless claims (exp. +2.5mm).

Market Structure: This weekend's COT positioning report showed larger-than-expected hedge fund selling in corn and a record fund net short position in spring wheat. Hedge fund positioning is looking more supportive in aggregate after five consecutive weeks of macro-driven fund selling; funds are extended short in corn, cattle, feeder cattle, sugar #11, and robusta coffee.

Momentum traders: CTAs have largely covered shorts over the past two weeks on upward momentum, but still hold big short positions in corn, spring wheat, arabica coffee, and robusta coffee.

What Matters This Week:

For today and most of tomorrow we countdown to the WASDE report at 18:00 GVA, 11:00am Chicago. After that, we go back to focusing on positive price seasonals and macroeconomic crosscurrents.

For price seasonals, traders are looking for some catalyst that gives the bullish May seasonal trend some traction: planting delays (today's planting progress report will confirm that window is closing fast), weather, exports, ethanol prices, south american dryness...something that pushes prices higher and washes out shorts like May '19.

Corn and spring wheat are worth keeping an eye on - both markets have big short positions (spring wheat is record net short today) heading into this seasonally bullish period. Both markets have plenty of vulnerable shorts.

For the macro environment, investors will be watching headlines around U.S.-China phase one trade deal commitments and the first look at May data via U.S. jobless claim numbers on Thursday. Price action matters, especially crude oil (firmer last week) and U.S. dollar (mixed after NFP).

Watch this week:

Any U.S. planting / weather catalysts that give May seasonals some traction.

Price action in energy / ethanol markets and U.S. dollar performance (USD down = Ags up)

U.S. data, especially jobless claim numbers on Thursday, our best "live" look as U.S. employment.

Chart of the Week: We’re in the most seasonally bullish weeks of the year for corn, wheat, and soybean meal. These are the weeks when planting delays and bad weather can negatively impact U.S. production and drive agriculture futures higher. Our seasonal heat maps calculate price strength on a +5/-5 scale basis 10 years of front-contract prices.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.