COT Market Participants (Hedge Funds Matter!)

Hedge funds really matter for commodity markets.

When hedge funds buy, prices go up and when hedge funds sell prices, go down.

Today we'll talk about who these hedge funds are, how they trade, and how we can see the influence that these funds have on commodity markets in the weekly Commitment of Traders reports.

We'll also talk about some other important investor categories: index funds, commercial traders, small private traders, and how they all interact with one another to exert influence over commodity market prices.

To get started, let's look at the big picture and talk about the four main participants in commodity markets.

That's hedge funds, index funds, commercial traders, and smaller private traders.

HEDGE FUNDS

Let's start with hedge funds. You probably know what a hedge fund is. It's an investment fund that is trying to make money for its clients by speculating. For commodity futures, a hedge fund is trying to either buy or sell short commodity futures with the goal of making a profit for its clients.

Rhere are a lot of different hedge funds that use a lot of different information and price drivers to trade but broadly speaking, they fall into three main buckets:

Systematic traders

Fundamental traders

Macro traders

Systems traders are mostly using some combination of technical or momentum signals to trade.

Fundamental traders are using balance sheets, e.g., how much of a crop is grown, how much it's harvested, how much demand there is.

Macro traders are taking big-picture thematic views, for example, a view on the dollar or a view on inflation and expressing that via commodity futures.

There's been an important trend in the last 10 years and that is hedge funds are focusing more and more on non-nonfundamental trading inputs (momentum, seasonality, macro flows) and less on fundamental trading inputs (yields, production, demand).

Who are some of the big systematic hedge funds in commodity markets?

It's groups like Millennium, Winton, Two Sigma, Systematica, and Square Point.

And some of the fundamentally-biased hedge funds like Citadel or DE Shaw are using a ‘quantamentals’ approach to trade. They're blending quant style trading with fundamental inputs that they can backtest.

Now, how do we know that hedge funds have so much influence in commodity markets?

If we look at weekly CFTC Commitment of Trader report money flows, we can see that there's a positive correlation between the money that hedge funds are putting into or out of commodity markets and what prices do during the week. If hedge funds buy, prices go up. If hedge funds sell, prices go down.

Now let's take an example from a big liquid agriculture market like corn.

If we take the correlation between hedge fund flows and prices, we can see that they are strongly positively correlated. Meaning again, when hedge funds buy, prices go up.

We can see that mathematically, we can prove that out. And this is the same for most commodity markets.

Hedge funds are the price drivers for commodity markets.

POSITIVE CORRELATION SHOWING HEDGE FUNDS AS PRICE DRIVERS

In our third article on Commitment of Traders reports, we’ll talk more about building real systematic trading systems around COT data. We’ll give real examples of how we can use hedge fund positioning to inform profitable trading decisions in real-time.

INDEX FUNDS

Let's move on to index funds.

Index funds invest in commodities as a hedge against future inflation. They're using commodity futures as a store of value. Examples of index fund investors: pension funds, endowments, foundations, and sovereign wealth funds. These groups have a big pool of assets that they need to protect against the threat of inflation.

POPULAR COMMODITY INDEX FUNDS

These index investors will invest in a commodity index, a popular index like the Bloomberg Commodity Index or the Goldman Sachs Commodity Index, where the goal is to just hold a big bucket of commodities, e.g., crude oil, gold, copper, silver, corn, wheat, soybeans, cattle, and cocoa.

They just want exposure to the whole commodity asset class so that if prices start rising, they know that they have a hedge against inflation.

As you might have guessed, the number one trading input that index investors use when deciding to put money into or out of commodity markets is future inflation expectations.

If they think inflation's going to run hot over the near term, they're going to put more money into commodities as a hedge against future price rises.

What are some examples of index investors?

California Public Employee Retirement System

Harvard Endowment

Abu Dhabi Investment Authority

These are investors that are investing for multiple quarters or even multiple years.

They're long-term, slow-moving investors.

COMMERCIAL TRADING HOUSES

Now the third category is the commercial or producer category.

These are big commercial trading houses like the ABCDs: ADM, Bungee, Cargill, and Louis Dreyfus.

Commercial trading houses are generally price takers in commodity markets. Remember, we talked about hedge funds being the price drivers, commercial trading houses are usually the price takers.

Now, this does *not* mean that commercial traders are uninformed or slow. What it does mean is that they usually have cash positions against their future trades. These producers might view futures as expensive or cheap basis cash and they're more willing to take the other side of the trade that hedge funds have on.

If we look at the correlation between weekly producer and commercial flows and price changes, we can see this relationship: there's a strong negative correlation in a market like corn. When producers buy or sell, it doesn't have the same positive correlation as hedge funds.

Producers are the price takers.

Negative CORRELATION SHOWING index FUNDS AS PRICE takers

SMALL PRIVATE TRADERS

Now let's talk about this final category, the fourth category, that's small prop shops.

In the disaggregated COT report, there's this category called other reportables.

Other reportables are a mix of groups that trade a significant number of contracts but they're not managing money for other groups…they're managing their own money.

Other reportables are:

Option locals

Family offices

Chinese speculators

And finally, there are non-reportable traders.

Non-reportable traders hold a small enough position in commodity futures that they fall below the CFTC's reporting requirements.

Here is where you can find what exactly these limits are for each market (scroll to section 15.03):

The CFTC is trying to ensure the orderly functioning of markets. The CFTC doesn't want a few big players colluding to run markets up and down and squeeze everyone out.

If you’re a small trader and you hold five contracts of corn or ten contracts of crude oil, the CFTC isn't too worried about you running markets or causing any disruptions…they just don't need to hear from you so they put you in the non-reportable category.

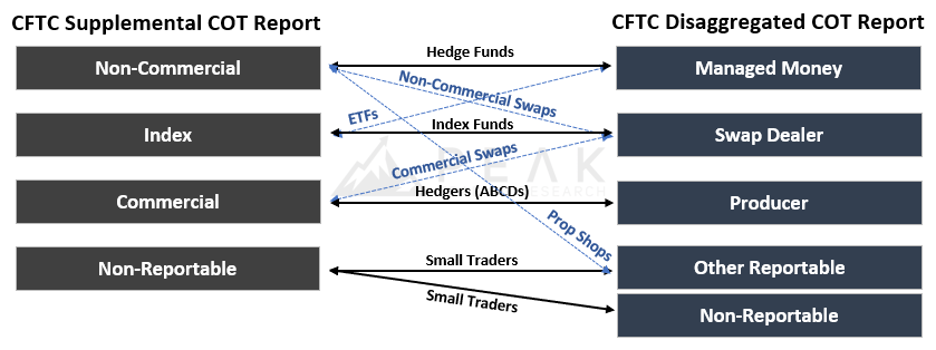

To helps clarify things a bit, here are some of the differences between how investors are mapped between the two different COT reports (Disaggregated and Supplemental):

CFTC REPORT COMPARISON: SUPPLEMENTAL VS. DISAGGREGATED

Before you get too confused, remember to focus on the big picture:

Hedge funds are the price drivers in commodity markets.

Now for some markets, index funds can matter a little bit more or other reportable traders can matter a little bit more but by and large, keep in mind that hedge funds are the price drivers.

That is the group that you really need to focus on.

We'll come back to this idea a lot in our third article, where we talk about building real systematic trading systems around COT data and specifically around hedge fund position.

Peak Trading Research is the only research company that provides its clients with quarterly updates of correlations between price changes and weekly COT money flow so you can always see the evolution of which category matters most in your trading.

CORRELATIONS BY MARKET

As always, if you're interested in a trial of our actionable commodity research, you can reach out, insight@peaktradingresearch.com.