Ag Markets August 31, 2020

Agriculture futures face strong crosscurrents coming into this week: bullish fundamentals (U.S. drought) and a supportive macro environment have driven hedge funds to add to extended-long positions and lifted prices against the negative August & September seasonal trend.

The macro environment is a positive trading input for agriculture futures coming into this week:

Last Thursday Fed chairman Powell announced that the Fed will adopt an "average inflation target" and will be more willing to let inflation run above the Fed's 2.0% target going forward.

Powell's announcement weakened USD and lifted inflation expectations through the end of last week, a positive boost for ag prices.

Index funds bought another +16k contracts of agriculture futures last week, chasing the inflation trend (chart of the week below).

Hedge fund positioning is an increasingly negative trading input looking forward:

Friday's COT positioning report showed +112k contracts of aggregate fund buying, the fourth largest inflow week of 2020. Funds have bought ag futures in nine of the past ten weeks.

Non-commercial traders are the longest they've been since May 2018, when Trump's China tariffs were first put in place.

Canola seed, soybeans, and robusta coffee are the most overbought markets across the ag complex (z-scores > +2.5).

CTA momentum traders are the longest they've been in 2020. Momentum traders in corn are the longest they've been since the prevent plant move in July 2019.

Price seasonals are a negative trading input, but we're nearing some important inflection points:

The seasonal low for each grain and oilseed market basis the past 10 years:

Corn: August 29th (two days ago)

Chicago wheat: September 2nd (this Wednesday)

Soybeans: September 27th

Soybean Oil: September 27th (before the annual low November 17th)

Soybean Meal: October 2nd

The seasonal low for the entire ag complex is September 27th; there is still time for prices to settle lower, especially in the oilseed complex...a lot of which will depend on weather and next week's big WASDE report.

What matters this week:

Agriculture markets have a strong fundamental story and hedge funds have gotten long, including CTA momentum traders. Traders are focusing on crop conditions, crop tours, china buying, and weather maps to gauge how tight this year's corn and bean SNDs can get. Non-fundamental inputs have taken a back seat (especially seasonality) after enjoying a great run since the prevent plant flooding 14 months ago.

The questions for agriculture traders this week:

Is midwest soybean and corn damage bad enough and the macro inflation story strong enough to justify this price run-up and hedge fund length?

How much further can we stretch the fund positioning rubber band...especially against September seasonals (the most *negative* month for soybeans)?

Watch this week:

On the fundamental side, tonight's crop condition scores, crop tour feedback, and China sales will move markets ahead of next Friday's WASDE report.

Macro focus is on U.S. job numbers: ADP Wednesday, jobless claims Thursday, NFP Friday. The next Fed meeting is in two weeks, September 15-16th. Markets are in risk-on mode, look to see if a weaker USD and higher inflation expectations can continue to support commodities this week.

Chart of the Week: Inflation matters for agriculture markets. Index fund investment in agriculture futures has moved in lockstep with inflation expectations over the past four months. Today agriculture markets have both a fundamental story (U.S. midwest drought) *and* an inflation story (new Fed inflation target policies)…a bullish combination.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets August 24, 2020

Hedge funds have been on a buying spree in agriculture futures.

Funds have bought agriculture futures in seven of the last eight weeks and this weekend's COT positioning report showed +232k contracts of hedge fund buying, the largest aggregate inflow week since January 2018.

Hedge funds are now the longest they've been in two years, with extreme long positioning in soybeans (second largest inflows on record last week), canola seed (near record long), and robusta coffee (longest in three years). There are now eleven markets that look expensive & overbought versus data from the past 24 months (chart of the week below).

This stretched positioning looks increasingly vulnerable given negative seasonal pressure in late August and September (especially for oilseeds) and as the macro environment is showing a few cracks: stronger USD, weaker BRL, crude oil settling lower.

Macro focus this week is on the Fed Annual Symposium and Republican convention:

Monday: Fed's annual Economic Symposium begins (normally held at Jackson Hole), Republican national convention kicks off in Charlotte and Washington DC.

Thursday: Jobless claims data (exp +1.0mm) and continuing claims (exp 14.4mm), Powell speaks on the Fed's policy framework, Trump speaks from the White House.

Markets are trading with a mixed tone this morning after Trump's announcement that the FDA has approved convalescent blood plasma as a Covid-19 treatment.

What matters this week:

Funds are extended long, seasonals are negative, and the macro environment is losing some shine. This is a bearish combination of trading inputs looking forward.

The question for agriculture traders this week: Can speculation around midwest crop damage and strong China demand keep grains and oilseed markets propped up against the weight of extended positioning, negative seasonals, and a less-rosy macro?

As a reminder, the seasonal low for corn is Aug 29th (this Saturday), chicago wheat Sep 2nd (next Wednesday), and soybeans Sep 27th.

Watch this week:

There isn't much data on the calendar this week; watch how the U.S. dollar reacts to Powell's comments on Thursday and watch price action in BRL and crude oil.

Also watch if funds (including long CTA momentum traders) start to take chips off the table, giving the late-August and early-Sep negative seasonal trend some traction.

Chart of the Week: Hedge funds have been on a buying spree in agriculture futures and today eleven agriculture markets look expensive and overbought versus data from the past 24 months.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets August 17, 2020

Hedge funds hold big long bets in agriculture futures, especially oilseeds and softs.

Funds have been on a buying spree for seven of the past eight weeks on a combination of:

Supportive macro environment (inflation up, USD down)

Chinese cargo demand and positive risk sentiment (A-shares up)

Last week's WASDE bounce

Iowa storm damage

Momentum trader buying

Today non-commercial hedge fund traders are the longest they've been in agriculture futures since January (chart of the week below).

This extended-long positioning matters, especially if some fundamental trigger (e.g. farmer selling) or non-fundamental trigger (e.g. strong USD) pushes prices lower and forces new longs to liquidate in markets like canola seed, robusta coffee, bean oil, and soybeans.

On the calendar this week:

Monday: Democratic convention starts in Milwaukee, Empire manufacturing data, crop ratings (Iowa #derecho damage).

Tuesday: U.S. housing starts data.

Wednesday: FOMC meeting minutes from the July 29th meeting.

Thursday: Weekly U.S. jobless and continuing claims data, Philly Fed data, Biden Dem nomination.

Friday: U.S., Eurozone, and U.K. PMI manufacturing data

Members of the U.S. House (and possibly the Senate) are returning to Washington D.C. early to address postal service funding. Investors are also watching the pace of U.S. Covid-19 infections, especially with more students heading back to school. Over the past two months more U.S. Covid cases vs other major currency nations = weaker USD = a positive driver for agriculture futures.

What matters this week:

Hedge funds are the longest they've been in six months and there are now ten agriculture futures markets that look expensive & overbought versus data from the past 24 months.

What keeps new longs confident and keeps prices elevated?

Positive macro (inflation up, USD down), China buying and Chinese risk sentiment (A-shares are testing cycle highs this morning), lower crop conditions today, dryer weather.

What could force new longs to liquidate, driving prices lower?

Negative macro (risk-off trading, USD up), better-than-expected crop conditions, confidence that the late-August & September seasonal trend is intact, farmer selling, CTA liquidations.

Ag markets have plenty of fundamental and non-fundamental crosscurrents to contend with this week. Big picture: funds are long (including momentum CTAs) and seasonals are negative for the next five weeks. These are both bearish trading inputs, esp if momentum slows and/or the macro environment sets back (e.g. stronger USD).

Chart of the Week: Today hedge funds hold big long bets in agriculture futures, playing for higher prices. These traders are the longest they’ve been since late January, before the big Covid-19 macro washout.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets August 10, 2020

Macro price action matters as we're entering a light data week ahead of Wednesday's WASDE report.

The supportive macro environment has propped up agriculture markets over the past month. Ag markets have benefited from strong risk-on sentiment, a weak U.S. dollar, and firm energy markets.

On Friday we saw what happens when that positive macro support is removed. The U.S. dollar strengthened +0.7% on better-than-expected NFP job numbers and wheat dropped -1.1%, beans -1.2%, cotton -3.8%, sugar no. 11 -2.1%. A reminder that USD up = ags down.

Price seasonals are broadly negative in August and September and hedge funds have added new long positions over the past six COT weeks. Extended-long and seasonally-negative markets like canola seed, feeder cattle, arabica coffee, robusta coffee, and sugar no. 11 look vulnerable if the macro mood worsens and the U.S. dollar recovers.

Note: Negative price seasonals, big production numbers, and negative carry are reasons why agriculture futures haven't kept up with equities. The ags vs equities ratio is making new all-time lows this morning (chart below).

On the calendar this week:

Wednesday: WASDE report, U.S. CPI inflation (exp +0.3%)

Thursday: Jobless claims data (exp +1.1mm) and continuing claims (exp 15.8mm)

Friday: U.S. retail sales, Chinese retail sales and industrial production

There's also questions regarding the legality and efficacy of Trump's stimulus executive order, headlines around Chinese app and IP bans, and U.S. Covid-19 cases breaking 5 million. Over the past month more U.S. Covid cases = weaker USD.

What matters this week:

The questions for agriculture traders:

Beyond Wednesday's WASDE volatility - can the macro environment hold up ag markets against the weight of negative seasonals and increasingly stretched fund positioning?

How much damage could a strong dollar do to ag futures...especially for overbought markets like canola seed, feeder cattle, sugar, and robusta coffee, sugar?

Watch this week:

Macro price action matters. Watch the path of the U.S. dollar and watch how Chinese markets (A-shares and CNY) react to Chinese data on Friday.

Chart of the Week: Equities have rallied more than agriculture futures over the past five months, pushing the ags vs equities ratio to new all-time lows this morning.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets August 3, 2020

What's the most bullish non-fundamental driver for agriculture markets this week?

U.S. dollar weakness. The U.S. dollar returned -4.2% in July, its worst month since April 2011. This USD weakness has been a powerful positive lever for agriculture futures and commodities broadly.

Why has the U.S. dollar weakened so much?

The U.S. has a higher rate of Covid-19 cases/deaths versus other major currency nations, which will keep U.S. interest rates low and keep Fed stimulus pumping, a negative driver for USD.

What's the most bearish non-fundamental driver for agriculture markets this week?

There are two big ones: Fund positioning and price seasonals.

Fund positioning: Hedge funds have been on a buying spree in agriculture futures over the past six weeks and today:

Non-commercial traders are the longest they've been since late Jan.

Momentum CTAs (~25% of funds) are the longest they've been since mid-Jan.

Hedge funds have less buying firepower looking forward, especially in broadly overbought markets like soybeans, bean oil, sugar no. 11, canola seed, feeder cattle, and arabica coffee.

Price seasonals: negative for grains, meats, sugar, and arabica coffee.

The annual low for corn is Aug 29th, chicago wheat Sep 2nd, soybeans Sep 27th. We're in the fourth quarter of the ag complex downdraft that runs from June 1st to Oct 1st.

What's on the macroeconomic calendar this week?

Monday: U.S. ISM manufacturing data, Tyson earnings.

Tuesday: U.S. durable goods data, BP earnings.

Wednesday: Brazil interest rate decision, ADP jobs (private survey preview of NFP jobs)

Thursday: Glencore earnings, jobless claims data (last week showed a second consecutive *increase* and the biggest jump in continuing claims since May), BOE rate decision.

Friday: Monthly U.S. nonfarm payrolls data, exp. +1.6mm jobs, unemployment ~10.5%.

What matters most for agriculture futures this week?

The U.S. dollar's next move matters for ags. A weaker U.S. dollar has been the #1 positive macro driver for agriculture markets over the past month. Hedge funds have bought futures and prices have risen. These new longs will look vulnerable if the U.S. dollar re-strengthens.

What macro catalysts could make the U.S. dollar strengthen?

#1 Better U.S. data. Lower jobless claims Thursday and better NFP jobs Friday would boost USD.

#2 U.S. Covid-19 cases and deaths dropping. U.S. cases down = USD up.

#3 Dovish non-U.S. central banks, e.g. if Brazil cuts rates on Wednesday

And if USD strengthens, ags will go down?

That's very likely. USD up = ags down...especially against the backdrop of newly added hedge fund longs and broadly negative price seasonals. A weaker USD propped up our markets in July (chart of the week below). Watch USD closely this week - especially around this week's jobs data and central bank decisions.

Chart of the Week: U.S. dollar weakness is a powerful positive lever for commodities broadly. USD just had its worst month since April 2011 and 20 out of 26 agriculture futures markets finished the month higher.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets July 27, 2020

This is a big macro week for agriculture traders: Fed policy decision on Wednesday, the U.S. government working on more fiscal aid, weekly jobless claims data on Thursday, and earnings announcements from big tech names (GOOGL, AAPL, AMZN).

The macroeconomic environment has been a supportive trading input for agriculture futures over the past month, largely driven by a lower U.S. dollar and higher inflation expectations. The rosy macro mood (and great U.S. export sales) has thrown agriculture futures a lifeline during what is normally a seasonally bearish time of the year for grain and oilseed markets.

With Chinese trade war tensions re-emerging (Houston and Chengdu consulates closed) and risk assets lower on Thursday and Friday last week, the macro environment will again be an important x-factor for agriculture futures this week.

Hedge fund positioning is becoming more of a bearish trading input looking forward. This weekend's COT report showed a fourth consecutive week of fund inflows (mostly bean oil) and today funds are the longest they've been since mid-February.

Price seasonals remain firmly negative for grains and oilseed markets. Chicago wheat prices have dropped in 12 of the past 12 years over the seven weeks following July 31st (chart of the week below).

What Matters This Week:

Agriculture markets face two significant non-fundamental headwinds this week: price seasonals are negative and hedge funds have built vulnerable longer-than-average positions in markets like chicago wheat, soybeans, bean oil, canola seed, and arabica coffee.

The question for agriculture traders this week: Can the macro environment hold up ag markets against the weight of seasonals and structure? What if the dollar re-strengthens on better data, fewer Covid-19 deaths, flight-to-safety flows, or a hawkish Fed on Wednesday?

Watch this week:

Structure: How vulnerable are new fund long positions? Will bean oil prices drop after this past week's big inflows (as they have after 15 out of 19 past big inflow weeks since 2010?)

Seasonals: Will negative seasonals weigh on expensive and overbought markets like chicago wheat, soybeans, and bean oil?

Macro: How will the U.S. dollar react to this week's Fed policy decision, U.S. data, and U.S. fiscal stimulus announcements? Will a weaker U.S. dollar remain the only positive macro trading input for agriculture futures?

Chart of the Week: Chicago wheat prices have dropped in 12 of the past 12 years the seven weeks following July 31st (this Friday)…will this year be different?

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets July 20, 2020

Hedge funds have been on a buying spree for the past month and fund positioning in agriculture futures is now a more bearish trading input looking forward:

The COT reports from June 30th and July 7th showed the biggest hedge fund inflows of 2020, this weekend's COT report (July 14th data) showed small inflows, and this coming Friday's COT will likely show additional fund buying.

Non-commercial fund positioning in agriculture futures is the longest since mid-February.

There are now seven markets that look expensive and overbought versus data from the past 24 months: soybeans, chicago wheat, soybean oil, matif rapeseed, canola seed, feeder cattle, and white sugar (chart of the week below).

Price seasonals are firmly negative - agriculture prices usually trend lower in the last weeks of July.

Expensive and overbought markets like chicago wheat, soybeans, and bean oil make attractive shorts given the persistent negative seasonal trend looking forward...there is a lot of air beneath these markets until the next seasonal inflection point ~October 1st.

The macroeconomic environment is a neutral trading input heading into this week:

Macro price action is sending mixed signals:

Good for ags: strong inflation expectations, U.S. stock markets up, USD down.

Bad for ags: weak South American currencies, low growth expectations.

On the calendar this week:

Q2 earnings ramp up (Microsoft, Unilever, UBS, Coca-Cola, Tesla).

Covid-19: the U.S. Senate has a two-week window to negotiate new packages (possible payroll tax deduction) before the August recess. U.S. deaths approaching 150k.

U.S. jobless claims and continuing claims data this Thursday.

Central banks are quiet this week; the next Fed policy decision is next Wednesday, July 29th.

What Matters This Week:

The question for agriculture traders this week: Was last week's rally a counter-seasonal blip...or are hedge funds adding length in anticipation of a more structural uptrend?

The macro environment is an important x-factor this week. If crude oil tips over or USD re-strengthens, markets like chicago wheat, soybeans, and bean oil look especially vulnerable from a negative seasonals + bearish structure standpoint.

Watch this week:

Seasonals: Will the strongly negative late-July seasonal trend pull expensive and overbought markets like chicago wheat, soybeans, and bean oil lower?

Macro: Are positive inflation expectations and better overall risk sentiment enough to bring some structural money back into agriculture markets? Watch U.S. stimulus negotiations this week, watch any U.S.-China trade headlines, and watch price action in S&P / Crude / USD.

Chart of the Week: Hedge funds have been on a buying spree over the past month and there are now seven agriculture markets that look expensive and overbought: soybeans, chicago wheat, soybean oil, matif rapeseed, canola seed, feeder cattle, and white sugar.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets July 13, 2020

Negative price seasonals are the primary non-fundamental price driver for agriculture futures coming into this week. The macro environment is a neutral trading input and fund positioning is a slightly bearish input (especially for soybeans) after the two biggest hedge fund inflow weeks of 2020.

Seasonals:

Price seasonals are a strongly negative trading input for most agriculture markets in July; futures prices tend to drop as agriculture traders remove the risk premium around U.S. production.

Several seasonal price patterns illustrate this strongly negative trend (full list sent to Peak clients this morning), including a strongly negative trend in soybeans: soybeans have sold off in 15 of the past 18 years the 6 sessions starting July 15th (chart of the week below).

Macro:

The macroeconomic environment is a ~neutral trading input: China sentiment has boosted agriculture futures (A-Shares up, CNYfx up), but other risk indices look more mixed, and SA currencies are a negative headwind.

It's a busy week for economic data and Thursday is a big macro day: Chinese Q2 GDP, ECB meeting + Lagarde press briefing, and U.S. jobless claim #s + U.S. retail sales.

Q2 earnings season ramps up this week, especially for banks: JPM, BAC, WFC, GS, C, MS

Covid-19: U.S. cases are still trending higher as states are figuring out how to get students back to school safely and unemployment bonus payments end in three weeks.

This weekend's COT positioning report (July 7th data) showed non-commercial fund traders bought +152k contracts, the largest aggregate inflow week of 2020. Corn still looks oversold, even after two weeks of big fund short covering. Soybeans is still the most overbought agriculture market.

What Matters This Week:

The question for agriculture traders this week: Late July seasonals are the most negative of the year...what positive fundamental or non-fundamental driver could offset this downward pressure?

Watch this week:

Seasonals: Will the strongly negative July seasonal trend gain traction this week?

China has been a positive driver for agriculture futures; will Phase 2 trade deal pessimism, Chinese GDP data, or U.S.-China military tensions derail this positive trajectory?

Dollar: Watch the ECB announcement and U.S. data on Thursday; the U.S. dollar has been weak lately; any re-strengthening would be an additional headwind for agriculture futures. USD up = ags down.

Chart of the Week: There are several negative seasonal price patterns in agriculture futures over the coming weeks, including soybeans. Being short November beans for the six sessions after July 15th (this Wednesday) has been a profitable trade in 15 of the past 18 years:

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets July 6, 2020

Agriculture traders see negative price seasonals versus a positive macro environment coming into this week, ahead of Friday's big WASDE U.S. production & demand report.

Seasonals:

Price seasonals are a strongly negative trading input for agriculture futures in July.

These are the weeks when agriculture traders gain more confidence around summer weather and quickly remove the production risk premium from U.S. futures prices.

Prices tend to drop sharply after the July 4th holiday; Peak’s normalized seasonality charts point sharply downward for most grains and oilseed markets (chart of the week below).

Macro:

The macroeconomic environment is upgraded to a positive trading input for ag futures.

Over the past week China sentiment has improved (A-shares up, CNYfx up), energy markets are stronger (crude ~$43/barrel), and inflation expectations have risen...all good things for agriculture markets.

Investors are weighing solid U.S. NFP employment numbers and great China data versus the negative impact of accelerating Covid-19 cases.

There isn't much data on the calendar this week. Q2 earnings season ramps up for the big U.S. banks next week.

The CFTC's COT positioning report comes out later today at 21:30 GVA, 4:30pm Chicago. This will be an interesting one: the data covers the June 30th stocks report rally in grains and oilseeds.

What Matters This Week:

The question for agriculture traders this week: For how long can the upgraded macro mood keep pushing agriculture futures higher against the strongly negative seasonal trend?

China data has improved, and China's U.S. corn and soybean buying are fundamental positives...but at what point do ag traders decide that the U.S. production window has closed and start trading burdensome balance sheets?

If you're long futures today and playing for higher prices in corn, wheat (the most seasonally accurate market of 2020), and soybeans, the calendar is not your friend. Grain and oilseed prices will likely be lower by October 1st...it's all about timing the turn.

Watch this week:

Seasonals: Ag markets got their late-June seasonal bounce, how quickly will the strongly negative July trend gain traction?

Macro: Can risk assets maintain escape velocity versus the gravity of more Covid-19 cases? Data is light this week, price action matters: watch China markets, watch crude, watch USD.

Today's holiday-delayed COT report. How much did funds cover last week? Did corn shorts get washed out? How long are funds in soybeans?

Chart of the Week: Grain and oilseed prices tend to drop sharply in July. We’ve seen this trend over the past ten years and last year, 2019, was no exception.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets June 29, 2020

The macroeconomic environment is a negative headwind for agriculture markets heading into this holiday-shortened trading week and ahead of tomorrow's quarterly USDA stocks report.

Markets traded with a risk-off tone late last week as Covid-19 cases accelerated across U.S. sun belt states and the U.S. surpassed 40,000 new daily cases for the first time. From Wednesday to Friday the S&P 500 dropped -3.9%, crude oil fell -3.8%, and the U.S. dollar rose +0.8%...all headwinds for agriculture futures.

This week has some important macro catalysts:

Today: EU - UK Brexit trade deal talks

Tuesday: Fed Chair Powell testifies before the House Financial Services Committee

Wednesday: ADP jobs, ISM manufacturing, FOMC meeting minutes (June 10th meeting)

Thursday: U.S. jobless claims, continuing claims, and the big June NFP payrolls report (a day early due to the Friday market holiday); NFP jobs exp +3.0mm, unemployment 12.4%

Friday: U.S. Independence Day market holiday

Beyond the negative macro environment, price seasonals are broadly positive this week before turning strongly negative in July.

This weekend's COT positioning report (June 23rd data) showed small hedge fund net outflows. Funds have now sold agriculture futures in 10 of the past 12 COT reports and hedge funds are the shortest they've been in nine months. CTA momentum traders are the shortest they've been since the first Covid-19 macro washout in mid-March (chart of the week below).

What Matters This Week:

The negative macro mood is overwhelming late-June's bullish seasonals and keeping hedge funds comfortably short in markets like corn, chicago wheat, kansas wheat, spring wheat, soybean meal, cattle, hogs, and robusta coffee.

Extended-short fund positioning is often a bullish contrarian indicator ("with funds so short, who's left to sell?"), but today the combination of negative macro, great U.S. weather, and negative upcoming July seasonals is keeping funds comfortably short. There just isn't a spark to push prices higher and force short stops today.

Watch this week:

Sentiment around Covid-19: This virus has been the #1 macro driver in 2020. Record Covid cases = more economic damage = macro risk-off trading = lower agriculture prices.

Data: U.S. employment data matters, esp this Thursday's "gold standard" NFP jobs report.

Price action: How will risk assets and the U.S. dollar respond to Powell’s testimony and the various job reports later in the week?

Seasonals: Can ags bounce before entering seasonally negative July? Or will the negative macro mood keep ag prices pinned to the mat like last week?

Chart of the Week: Momentum traders have quickly gotten short agriculture futures, partially driven by last week’s negative macroeconomic sentiment. Today these momentum CTAs are the shortest they’ve been in three months, playing for a continued downtrend in agriculture prices.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets June 22, 2020

There are two non-fundamental agriculture price drivers worth watching this week:

The macro environment has been a volatile trading input as investors weigh the positives of central bank stimulus and economies reopening versus Covid-19 second wave prospects.

The late-June seasonally bullish window for grain and oilseed prices, sandwiched in an otherwise seasonally bearish June 1st - Oct 1st period.

The macroeconomic environment has sent mixed signals for agriculture traders over the past week:

Positive for ags: higher energy commodity prices, higher inflation expectations, strong China sentiment, and higher EM stock markets.

Negative for ags: Weaker South American currencies, firmer U.S. dollar, and lower global growth expectations (reflected in lower interest rates and bond yields).

This week is a quiet week for data and central bank announcements. U.S. jobless claims and continuing claims data are on Thursday. Markets are trading with a mildly supportive tone this morning.

Price seasonals are broadly positive for ag futures in late June - prices tend to bounce. Peak's seasonal heat maps (chart of the week, below) are a sea of green for the next two weeks before turning dark red again in July.

What Matters This Week:

The macro environment is an important x-factor this week for agriculture markets.

If the macro environment turns more negative this week that would be a red flag for markets with newly added hedge fund length like soybeans, bean oil, and sugar.

If the macro pushes into positive territory, there are plenty of cheap and oversold markets that look like good value picks, especially in the context of a late-June seasonal price rebound: corn, kansas wheat, chicago wheat, soybean meal, cattle, hogs, and robusta coffee.

Watch this week:

Sentiment around Covid-19. This virus has been the #1 macro driver in 2020 and things are turning south again: CA record new cases, stores re-closing, second wave warnings.

Macro price action. There's very little on the data calendar this week. Watch S&P 500, crude oil, and the U.S. dollar (can Brazilian real re-strengthen?).

Will ag markets see a quick seasonal bounce? This is especially relevant for oversold markets with big CTA short positions like chicago wheat, soybean meal, and coffee.

Chart of the Week: Is it time to buy chicago wheat and soybean meal? Price seasonals are briefly positive for grain and oilseed markets in late June…a small break from the seasonally-negative trend that runs from June 1st to October 1st.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets June 15, 2020

The macro environment is losing momentum after a positive start to the month of June.

Last week the S&P 500 dropped -4.8%, crude oil -8.4%, BRL -1.8%, and BCOM Ags -1.3%.

This morning S&P futures and crude oil are trading lower.

This macro move matters for ag markets, especially in the context of broadly negative price seasonals for agriculture markets from June - September.

If the macro environment turns more negative (crude down, S&P 500 down, USD up), that means two big price headwinds for ags markets: macro and seasonals.

Last week we got a glimpse of what that looks like: 23 of 26 agriculture futures markets finished the week lower. See the chart of the week below.

This week is a busy week for macro data and central bank announcements:

Monday: U.S. Empire manufacturing, CBOE trading floor open.

Tuesday: Bank of Japan policy decision, Fed Chairman Powell's Senate banking committee testimony, U.S. retail sales and industrial production.

Thursday: Bank of England policy decision (more bond buying?), Swiss National Bank policy decision, and U.S. jobless / continuing claims

Saturday: Trump's first Covid-era live campaign in Tulsa, Oklahoma.

Investors will also be balancing the upside from businesses reopening versus evidence that Covid-19 cases are accelerating. Arizona, Arkansas, Alabama, North Carolina, and Oklahoma reported record new cases last week.

Investor positioning: This weekend's COT report showed that hedge funds have sold ag futures in nine of the past ten weeks. Hedge fund positioning is becoming a more bullish trading input and funds are extended short in markets like corn, spring wheat, cattle, and hogs. Corn is the most oversold market across the ag complex.

What Matters This Week:

Seasonals are a negative trading input and will remain that way for the next four months. As a reminder, the ag complex seasonal high last year, 2019, was June 17th = this Wednesday. If you're long grain and oilseed futures for fundamental reasons, the calendar is not your friend.

The macroeconomic environment is an important x-factor this week:

Positive macro (S&P up, crude up, USD down) = an offset to negative price seasonals.

Negative macro (S&P down, crude down, USD up) = an acceleration of negative price seasonals = ag markets drop further...like last week.

Big Picture: Macro direction matters this week, seasonals are a headwind, and hedge funds have gotten shorter, especially in corn.

Watch this week:

Investor sentiment: businesses reopening vs Covid-19 "second wave" acceleration.

Watch Powell's testimony, BoJ and BoE policy decisions...all are important USD drivers.

Will price seasonals keep pressing ags lower? Will investors continue to remove a price risk premium from our markets ahead of the big June 30th stocks report later this month?

Chart of the Week: Macro matters. Last week the macroeconomic mood soured (S&P 500 -4.8%) and 23 out of 26 ag markets finished the week lower.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets June 8, 2020

Last week's risk-on macro trading flipped all the right switches for agriculture futures: crude oil +11.8% on the week, S&P 500 +4.9%, Brazilian real +7.6%, and, importantly, U.S. dollar index down -1.4%. The BCOM Agriculture subindex rose +2.8% on the week to its highest level in two months.

Friday's much better than expected Nonfarm payrolls report (+2.5mm jobs vs -7.5mm exp.) helps set a positive trading tone for the coming weeks. Also this weekend: OPEC and Russia extended crude oil production cuts, another positive for energy-linked ags like corn, bean oil, and sugar.

Price seasonals are a headwind and remain negative for the next four months; ag prices tend to drop from June 1st to October 1st. The ag complex seasonal high last year, 2019, was June 17th = next Wednesday.

It's not just the corn, soy, and wheat markets that see negative seasonal pressure - cotton futures have dropped in 12 of the past 12 years during these coming three weeks. Chart of the week below.

Hedge fund positioning is mixed by market but generally a bullish trading input. This weekend's COT report showed that hedge funds have sold in eight of the nine past weeks and funds are extended short in markets like corn, meal, cattle, and hogs. Funds are *very* short corn: +5 MS score, -1.68 z-score.

What Matters This Week:

Macro momentum matters. If the macro mood remains positive - especially energy up, inflation up, USD down - there are plenty of cheap and oversold ag markets that make great value picks for optimistic macro traders.

Corn is the market with the most explosive upside from a positioning standpoint. Corn's massive 3+ billion bushel carryout is a long-term cement brick, but summer weather and/or price momentum could drive funds to cover shorts over the near-term.

Big Picture: Macro momentum matters, seasonals are a headwind for the coming months, and hedge funds are extended short in a few key markets, especially corn.

Watch this week:

Macro momentum. Watch Fed chairman Powell comments Wednesday.

Can agriculture markets maintain escape trajectory vs negative seasonal pressure?

Watch corn: funds are short (including momentum CTAs) and this recent rally hurts.

USDA WASDE report this Thursday ahead of the big June 30th stocks report later this month.

Chart of the Week: The macroeconomic environment has provided a big positive boost for agriculture futures this month, driving prices higher against the seasonally-negative June trend. Cotton futures prices have dropped in 12 of the past 12 years for the three weeks starting today…will the positive macro mood break this streak?

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets June 1, 2020

Agriculture markets cross an important seasonal threshold today:

Grain and oilseed prices tend to drop from June 1st to October 1st.

After June 1st, ag traders know enough about U.S. production prospects - planting progress, ground moisture, extended forecasts - to begin removing the price risk premium from corn, wheat, and soybeans.

For the corn market, we've seen prices drop from June 1st to October 1st in 3 of the past 3 years (chart of the week below), 6 of the past 7 years, and 14 of the past 17 years. It's a strong, consistent trend.

Last year, 2019, corn prices topped out on June 17th at $4.69/bushel (Dec contract) before dropping 81 cents (-17%) to $3.88/bushel by September 30th.

It's still a long growing season with plenty of time for bad weather to dent U.S. production (and funds hold a big short position in corn, which limits further downside selling) but the window for U.S. production problems is closing every day.

Bottom line: Price seasonals will be a headwind and negative trading input for the next four months.

Beyond negative price seasonals, agriculture markets see a positive mix of other non-fundamental factors:

Macro: Slightly positive for ags coming into this week. Trump's China conference on Friday removed the tail risk of quitting the Phase One trade deal and/or new sanctions. Today's combination of better risk sentiment + higher energy prices + weaker U.S. dollar = a great combo for ags. This is a busy data week: ISM Manufacturing surveys early in the week, ECB decision Thursday, May U.S. Nonfarm payrolls on Friday, exp. -8.0mm jobs, unemployment rate at 19.6%.

Market Structure: We've seen hedge fund selling outflows in seven of the past eight COT weeks; this weekend's COT report showed new fund shorts in corn, beans, meal, and bean oil. Fund positioning is a bullish trading input for extended-short markets like corn, soybean meal, cattle, and robusta coffee...especially if we see any bad U.S. midwest weather over the coming weeks.

Momentum traders: Like the broader market structure picture, momentum traders are short in aggregate, with big shorts in corn, chicago wheat, soybeans, meal, and coffee.

What Matters This Week:

Price seasonals are now a headwind for agriculture markets and will remain that way until early October. Ag markets see plenty of summer volatility over the coming weeks, but the price trend is generally lower.

Market structure is a bullish input as funds have gotten shorter over the past two months. Extended-short markets like corn have plenty of fund buying power *if* some trigger drives prices up and squeezes big short positions.

The macro mood is more positive this week. U.S. businesses are reopening and last week's drop in continuing jobless claims shows people are returning to work. George Floyd national protests are having a negative impact on USD (good for ags) but aren't impacting equities or energy markets for now.

Big Picture: Seasonals are now negative, but the macro environment has improved, and hedge funds are extended short in a few key markets, limiting downside.

Watch this week:

Will ag markets see seasonal short-selling flows in corn, beans, wheat?

U.S.- China tensions & tweets, can Chinese risk assets sustain upward momentum?

Big NFP jobs report this Friday, will U.S. dollar re-strengthen if data is better than expected?

Chart of the Week: Corn prices generally trend lower from June 1st - October 1st as traders gain more certainty around final U.S. production. We’ve seen this negative price trend in each of the past three years.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets May 25, 2020

Agriculture markets see mixed non-fundamental trading signals coming into this holiday-shortened week.

Seasonals: The seasonally bullish spring window is closing fast. May price seasonals are strongly positive but June seasonals turn more bearish as traders see extended weather forecasts and assign a lower risk premium to U.S. production estimates.

Macro: Positive risk sentiment faded on Friday when China abandoned their formal GDP target (A-shares down -1.9%) and the U.S. dollar strengthened on flight-to-safety flows, a headwind for agriculture futures. This week is quiet for scheduled data and central bank decisions; we'll see weekly U.S. jobless claims (exp. +2.1mm) on Thursday.

Market Structure: We've seen hedge fund selling outflows in six of the past seven weeks COT weeks; this weekend's COT report showed new fund shorts in corn, chicago wheat, kansas wheat (record managed money selling), soybeans, and meal. Fund positioning is a bullish trading input for stretched-short markets like spring wheat (record short), corn, cattle, meal, and robusta coffee.

Momentum traders: Like the broader market structure picture, momentum traders are short in aggregate, with big shorts in kansas wheat, soybeans, meal, and arabica coffee.

What Matters This Week:

Price seasonals turn more bearish after this week - that's a big change for our markets. Massive carryouts and hiccup-free U.S. planting have kept a lid on prices over the past weeks - we have not seen a seasonal rally like May 2019. It's still a long growing season (~90% of corn's yield determined in July), but the window for production problems is closing every day.

Although seasonals are less of a bullish input looking forward, market structure is becoming more of a bullish input as funds have gotten shorter over the past two months. Extended-short markets like spring wheat and corn have plenty of fund buying power *if* some fundamental (summer heat?) or non-fundamental (weaker USD?) trigger drives prices up and washes out shorts.

The macro environment remains a big x-factor for our markets and changes day-to-day with crude oil and the U.S. dollar.

Watch this week:

Can agriculture futures get a final seasonal push higher into June?

Price action in crude oil and ethanol, esp for energy-linked corn, bean oil, and sugar.

How the macro environment responds to escalating U.S.-China tensions, esp for China A-shares and CNYfx...both of which are highly correlated to ag futures.

Chart of the Week: Hedge funds have sold agriculture futures in six of the past seven weeks on a combination of bearish fundamentals and negative macro headwinds. Hedge funds have gotten comfortably short in markets like spring wheat, corn, cattle, and soybean meal. Spring wheat has record-short hedge fund positioning, with a positioning z-score of -2.12, the most negative across the ag complex.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets May 18, 2020

Agriculture markets see mixed non-fundamental signals coming into this week.

Price seasonals and hedge fund positioning are positive trading inputs, but a persistently strong U.S. dollar (especially vs BRL and CNY) is keeping a lid on our markets.

This week:

Price Seasonals: We're still in the most seasonally bullish weeks of the year for corn, chicago wheat, and soybean meal. This is the time of year when traders typically add a price risk premium to futures ahead of the big U.S. production months.

Macro: Crude oil breaking higher is a broadly positive input for agriculture futures, but the U.S. dollar remains stubbornly strong. Fed Chairman Powell testifies before the Senate Banking Committee starting Tuesday morning at 10am EDT with a message along the lines of "this recovery will take a while, the Fed is *not* considering negative rates but has plenty of other tools, more fiscal stimulus would help." We'll also see weekly U.S. jobless claims (exp. +2.5mm) and Philly Fed Thursday. China's annual NPC meetings kick off on Friday.

Market Structure: This weekend's COT positioning report showed small fund inflows, some surprise selling in corn, and a record net short position in spring wheat. Fund positioning is a bullish trading input for stretched-short markets like spring wheat, corn, cattle, and feeder cattle.

Momentum traders: Like the broader market structure picture (which includes all hedge funds, including momentum CTA traders), momentum traders have big short positions in a few markets like corn and spring wheat.

What Matters This Week:

The U.S. dollar is an important x-factor for our markets this week.

Seasonals are positive, market structure is supportive (esp for oversold markets like corn and spring wheat), and the rally in crude oil is a big boost for agriculture futures.

The U.S. dollar is up ~1.5% in May; if USD gives back some ground, that would make the macro environment more of a bullish trading input and we'd have some positive factor alignment from macro + seasonals + market structure.

To put it another way - what would be the most bullish combination of non-fundamental factors for ag markets this week?

Crude oil continuing to rally, a weaker U.S. dollar (watch Powell's testimony tomorrow), plus some seasonal spark that drives prices higher and triggers a short-covering wave in markets like corn and spring wheat.

Watch this week:

Any U.S. weather catalyst that gives May price seasonals some traction.

Price action in crude oil, esp for energy-linked markets like corn, bean oil, palm oil, and sugar.

How the macro environment reacts to Powell's testimony tomorrow and U.S. data Thursday; a weaker U.S. dollar would be a big boost for ag markets this week.

Chart of the Week: A structurally strong U.S. dollar has been a headwind for agriculture futures over the past year and the dollar’s +1.5% rally this month has blunted the positive impact from stronger energy markets (crude oil +23% in May) and improved risk sentiment (S&P 500 up, VIX down).

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

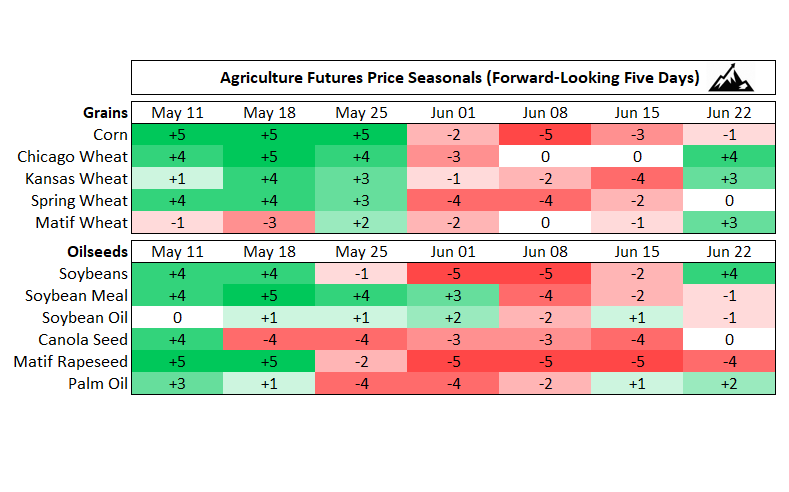

Ag Markets May 11, 2020

Tomorrow we see the USDA's big May WASDE report and the first look at crop year 20/21 balance sheets.

Beyond Tuesday's fundamental trading inputs, agriculture traders have plenty of non-fundamental inputs to consider:

Price seasonals: We're in the most seasonally bullish weeks of the year for corn, chicago wheat, and soybean meal. Yesterday, May 10th, was the seasonal low for the ag complex last year, 2019, and our seasonal heat maps (chart of the week, below) are a sea of green for the coming weeks.

Macro: Friday's U.S. Nonfarm payrolls report showed a record -20.5 million jobs lost in April (largely priced in after April's miserable weekly jobless claim reports). This week we see U.S. retail sales, CPI inflation, Empire Manufacturing PMI, and jobless claims (exp. +2.5mm).

Market Structure: This weekend's COT positioning report showed larger-than-expected hedge fund selling in corn and a record fund net short position in spring wheat. Hedge fund positioning is looking more supportive in aggregate after five consecutive weeks of macro-driven fund selling; funds are extended short in corn, cattle, feeder cattle, sugar #11, and robusta coffee.

Momentum traders: CTAs have largely covered shorts over the past two weeks on upward momentum, but still hold big short positions in corn, spring wheat, arabica coffee, and robusta coffee.

What Matters This Week:

For today and most of tomorrow we countdown to the WASDE report at 18:00 GVA, 11:00am Chicago. After that, we go back to focusing on positive price seasonals and macroeconomic crosscurrents.

For price seasonals, traders are looking for some catalyst that gives the bullish May seasonal trend some traction: planting delays (today's planting progress report will confirm that window is closing fast), weather, exports, ethanol prices, south american dryness...something that pushes prices higher and washes out shorts like May '19.

Corn and spring wheat are worth keeping an eye on - both markets have big short positions (spring wheat is record net short today) heading into this seasonally bullish period. Both markets have plenty of vulnerable shorts.

For the macro environment, investors will be watching headlines around U.S.-China phase one trade deal commitments and the first look at May data via U.S. jobless claim numbers on Thursday. Price action matters, especially crude oil (firmer last week) and U.S. dollar (mixed after NFP).

Watch this week:

Any U.S. planting / weather catalysts that give May seasonals some traction.

Price action in energy / ethanol markets and U.S. dollar performance (USD down = Ags up)

U.S. data, especially jobless claim numbers on Thursday, our best "live" look as U.S. employment.

Chart of the Week: We’re in the most seasonally bullish weeks of the year for corn, wheat, and soybean meal. These are the weeks when planting delays and bad weather can negatively impact U.S. production and drive agriculture futures higher. Our seasonal heat maps calculate price strength on a +5/-5 scale basis 10 years of front-contract prices.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets May 4, 2020

This week we enter the most seasonally bullish multi-week period of the year for corn, chicago wheat, and soybean meal. U.S. planting and production disruptions often occur in May and June; we saw this last year when U.S. Midwest flooding in May prompted record hedge fund short covering.

On the macro front, we're counting down to what will be a historic Nonfarm payrolls report on Friday at 14:30 GVA, 7:30am Chicago. The NFP report is expected to print -21.3 million jobs, with an unemployment rate of 16.0%. We'll see ADP jobs (the private survey version of NFP) on Wednesday and weekly U.S jobless claim numbers on Thursday.

Beyond the NFP print on Friday, there isn't much else on the macro calendar: Q1 earnings season is winding down (Tyson reports today) and the Bank of England has a policy decision on Thursday.

This weekend's COT positioning report showed small new short positions in corn, chicago wheat and sugar #11. The main takeaway from the COT report: hedge fund positioning is a neutral input overall, there isn’t a supportive positioning set-up like May 2019 when hedge funds were record short and vulnerable to a big short-covering squeeze heading into U.S. planting.

Although fund positioning is ~neutral in aggregate, agriculture prices are low. The BCOMAg index is near all-time lows this week and the agriculture vs equities ratio is back near the lows from February (chart of the week below).

What Matters This Week:

#1 Price seasonals and any weather problems that could negatively impact U.S. production. May is a seasonally bullish month and the spring seasonal low last year was May 10th (this coming Sunday).

#2 Macro price action and Friday's big NFP jobs report.

What would be the most bullish non-fundamental setup for ag futures?

If stronger energy prices and a weaker USD can make the macro positive and some fundamental negative catalyst around U.S. planting / production drives prices higher and washes out shorts in markets like corn, spring wheat, and soybean meal.

Watch this week:

Price action in energy markets and U.S. dollar performance (USD up = Ags down)

U.S. jobless claim #s on Thursday and NFP jobs Friday, both at 14:30 GVA, 7:30am Chicago

Any U.S. planting / weather issues that make positive May seasonals grip

Chart of the Week: Agriculture markets have underperformed stock markets due to low energy prices, a stronger U.S. dollar, and burdensome balance sheets. The agriculture vs equities ratio is testing all-time lows, matching levels last seen in February before the Covid-19 macro washout.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets April 27, 2020

The macroeconomic environment has been the #1 non-fundamental driver for agriculture futures over the past three months, with lower crude oil, lower inflation/growth expectations, and a stronger U.S. dollar pushing the ag complex to new 2020 lows today. The BCOM Ag Index is down -16.2% YTD.

On the macro front, this week agriculture investors will be focusing on:

Covid-19 curve-flattening progress and timelines to reopen global economies

Q1 earnings from big commodity names: BP, Shell, Exxon, Chevron, CAT, Glencore

Price action in energy markets after the WTI May contract expired negative last Monday

Additional central bank stimulus measures: BoJ today, Fed Wednesday, ECB Thursday

Price seasonals become a more positive price driver in the coming weeks as we get deeper into U.S. corn and soybean planting and traders add a risk premium to most ag markets. Basis 10yrs of front-contract prices, the spring seasonal low for corn was April 20th, last Monday, and coming up we have:

Soybean meal = May 2nd (this coming Saturday)

Chicago wheat = May 7th (next week Thursday)

Soybeans = May 10th

This weekend's COT positioning report showed new macro-driven short positions in corn, soybeans, bean oil, and sugar #11...all markets connected to crude oil prices via ethanol or biodiesel. Hedge fund traders have record-small long bets in Sugar #11 for a fifth consecutive week (chart below).

Our internal models show that momentum CTA traders, the most volatile slice of the overall hedge fund pie, are extended short. This extended-short positioning will matter if we see some macro or seasonal price driver that forces short covering, esp. for markets like corn, cattle, and bean oil.

What Matters for Ag Futures This Week:

The macro environment has been the #1 non-fundamental driver for agriculture futures but seasonals might soon take the #1 spot: this is the time of year when we see real threats to U.S. production. The seasonal low for the ag complex last year was May 10th, after which agriculture prices ripped higher on midwest flooding and lost acres.

The macro mood has improved over the past few trading sessions, with higher stock markets (good for risk sentiment) and firmer energy markets (good for ags). The U.S. dollar hit three-week highs last Friday but has backed off since. More USD weakness would help lift ag prices this week, esp if crude can hold > $20/bl.

Watch this week:

Progress on Covid curve flattening and concrete plans to open economies

Central bank policy tweaks (ECB optimism would push USD lower)

U.S. jobless claim #s on Thursday at 14:30 GVA, 7:30am Chicago; exp +3.5mm new claims

Any U.S. planting delays that suggest we've marked the seasonal low for the ag complex

Chart of the Week: The macroeconomic environment has been a significant headwind for sugar prices - especially lower energy prices (sugar is used to make ethanol) and a weaker Brazilian real. This weekend’s COT positioning report showed hedge funds have record-small long positions in sugar #11 futures for a fifth consecutive week. Sugar futures prices are at 12-year lows today.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.

Ag Markets April 20, 2020

What would drive agriculture futures prices higher this week? What makes ag markets broadly bullish?

Let's review the four non-fundamental "M" drivers for agriculture futures:

Macro

Month (seasonals)

Market Structure

Momentum (CTAs)

Macro: The macro environment is currently neutral for agriculture futures. The recent stock market rally is good for risk sentiment, which is good for ag futures prices. On the other hand, energy markets are weak (WTI below $16/barrel) and the U.S. dollar is stubbornly strong, which is bad for ag futures. What would make the macro environment a positive input for ags? Stronger crude and a weaker U.S. dollar (esp vs BRL, ARS, CNY).

Month: Price seasonals turn positive for ag futures in May...this is the month we flag big U.S. planting / production issues. The spring low across the ag complex last year was May 10th, and on average the spring low is:

Corn = April 20th (today, see the chart of the week below)

Soybean meal = May 2nd

Chicago wheat = May 7th

Soybeans = May 10th

Market Structure: Hedge funds are extended short in corn, live cattle, cotton, robusta coffee, and feeder cattle and fund positioning is potentially a bullish input for these extended-short markets...the caveat is that we need a trigger, i.e., some fundamental or technical change to drive prices up and squeeze shorts.

Momentum: Momentum and trend-following CTA traders are short across most markets and are max short in corn, soybeans, soybean meal, lean hogs, and robusta coffee. CTAs have plenty of firepower to buy futures in these markets.

Bottom Line:

Price seasonals *will* turn more bullish for most ag markets over the coming weeks.

The macro environment *could* turn bullish, but needs help from stronger crude / weaker USD.

Market structure (the whole hedge fund pie) and Momentum CTA trader positioning (the most volatile slice of the pie) are bullish inputs *if* either seasonals (planting delays) or the macro (weaker USD) can provide a spark and get prices moving higher, squeezing shorts and incentivizing new longs.

For the macro environment this week we see global Purchasing Manager Index (PMI) manufacturing data, U.S. jobless claims (exp. +4.5mm) and plenty of Q1 earnings from big commodity names: Alcoa, BHP Group, Anglo American. There's also a $450B U.S. small business loan program in the pipeline.

Chart of the Week: Corn futures cross an important seasonal inflection point today, April 20th. Corn futures prices tend to rise in late April and May as traders build in a risk premium around U.S. planting and production. Corn prices bottomed out on May 10th last year (2019), then rallied +30% in five weeks.

For a trial of our industry-leading agriculture research, reach out to us: insight@peaktradingresearch.com.