How Hedge Funds Make Money Trading Commodities: Momentum & Volatility

Hedge funds and Commodity Trading Advisors (CTAs) make money in commodity market futures by trading momentum and volatility. They buy markets that they hope will keep going up and sell short markets that they hope will keep falling. Today, we'll discuss how hedge funds trade and how we can see evidence of this in the market.

At Peak Trading Research, we specialize in quantitative commodity research and focus on modeling market participant behavior, especially quantitative traders like hedge funds and commodity trading advisors (CTAs). Most hedge funds and CTAs in commodity market futures are momentum traders, hoping to buy into a market that's rising, so they can sell at a profit.

For example, in February and March 2022, supply chains were tight, China was locking down with Covid, and commodity markets that were sensitive to Black Sea production or Russian exports, like wheat, crude oil, and natural gas, saw a rise in prices due to Russia's invasion of Ukraine on February 24th.

According to the weekly commitments of traders reports published by the US government, hedge fund speculators were buying into this upward momentum, and their aggregate investment in commodities across energy, metals, and agriculture markets got up to $170 billion by early March 2022, decade-high levels.

Peak Trading Research's proprietary CTA ladder model, which quantifies the aggregate positions and profits of momentum trading CTA traders, confirmed that most CTA traders were long commodity futures across agriculture, energy, and metals markets, making strongly positive profits.

The SocGen CTA Index and the SocGen CTA Trend Index, which capture the performance and profits of different CTA traders, also revealed that these commodity trading firms made a lot of money trading the momentum and big volatility in the spring of 2022.

A practical example of how a hedge fund might buy commodity futures on upward momentum is a simple momentum trading strategy on heating oil. This breakout strategy buys if the market is closing at the highest level of the past 20 price bars and sells short if it's falling.

The system has a stop-loss and will get out after 40 bars if there's no other trading signal. This strategy made about $180,000 per single contract of heating oil traded over the past five years, and its equity curve looks similar to the performance of the SocGen CTA indices.

Effectively, a very simple breakout momentum trading strategy on one market, on just the heating oil market is a great proxy for how this entire industry trades, buying upward momentum, hoping prices keep rising for a profit, selling short downward momentum, hoping prices keep dropping for a profit. That is these hedge funds’ ‘bread and butter’ trade.

In summary, hedge funds and CTAs position themselves to buy upward momentum, hoping prices keep rising for a profit and sell short downward momentum, hoping prices keep dropping for a profit.

We can see evidence of this in government positioning reports, Peak Trading Research's research, SocGen profitability indices, and a simple breakout trading system that acts as a proxy for the entire hedge fund industry.

Hopefully, you now have a great sense of how hedge funds and commodity trading advisors position themselves and make profits in commodity market futures.

If you'd like a trial of our quantitative commodity research, you can reach out Insight@PeakTradingResearch.com.

Commodity Index Rebalance Explained

The annual commodity index rebalancing is an important event for all commodity futures markets. During this time, the world's two largest commodity indices, the Bloomberg Commodity Index and the S&P GSCI Commodity Index announce their new weightings and rebalance their holdings to reflect those new weightings.

Index investors are major participants in commodity markets, making this annual rebalancing important for trader sentiment and commodity market prices during the rebalancing window in early January.

Index investors in commodity markets are generally investors who use commodity markets as a store of value or a hedge against inflation to protect the value of their portfolios. These groups include sovereign wealth funds, pension funds, and endowments, which invest in a combination of stocks, bonds, real estate, private equity, and commodities.

The two indices in focus are the Bloomberg Commodity Index and the S&P GSEI Commodity Index, with more than $200 billion in assets under management between them.

The two indices are similar in their aim to create a diversified and representative basket of commodity futures that investors can put money into. The key difference is that the GSCI index is production-weighted and more weighted towards energy, while the BCOM Index is production and liquidity-weighted and more broadly diversified. Both indices are liquid and easy to follow, and index investors invest in them both.

There are four questions that are most relevant for this annual index rebalancing:

Who are the investors that invest in these commodity indices? Index investors in commodity markets are generally investors that are looking to use commodity markets as a store of value, as a hedge against inflation to protect the value of their portfolios. These are often groups that have big pools of assets, for example, sovereign wealth funds or pension funds or endowments.

What are the differences between these two indices? The GSCI index is production-weighted and more weighted towards energy, while the BCOM Index is production and liquidity-weighted and more broadly diversified.

How does this rebalance work? The annual rebalancing occurs in early January, with both Bloomberg and S&P announcing their new index weightings in October or November. The rebalancing window occurs between the fifth and ninth business days of January, reflecting the new weights and the relative performance of each commodity market.

For which markets does the rebalance matter the most? While some traders argue that the annual index rebalance doesn't matter due to its predictability and the availability of different order types, others contend that it matters for markets with illiquid trade-at-settlement options or where these flows represent a large percentage of open interest or trading volume. Market sentiment is also affected when index investors are buying or selling a significant amount of contracts, particularly for markets where the index rebalance is a significant percentage of either volume or open interest.

Peak Trading Research clients receive weekly updates on the markets that are most vulnerable to these index rebalancing flows. These clients include index funds, hedge funds, family offices, private traders, and many of the largest commercial trading houses in the world. To quantify and anticipate these big index rebalancing flows every year, traders must manage their risk and consider the impact of index investors on commodity markets during this annual rebalancing event.

For a trial of Peak’s actionable commodity research, reach out to us at Insight@PeakTradingResearch.com.

How to Trade Seasonal Futures Price Moves

Commodity markets follow strong and consistent seasonal price trends. There are certain times of the year when futures prices tend to go up, and there are other times of the year when future prices tend to drop.

Today, we'll talk about why these consistently strong seasonal trends exist, the different ways that you can analyze these trends, and the most consistently profitable approach for trading these trends.

Let's start by reviewing what seasonality is.

Seasonality is an extremely important concept to understand to successfully trade commodity markets. At Peak Trading Research, we talk a lot about the four most important non-fundamental drivers for commodity prices:

Macro economic environment

Month (aka seasonals)

Market Structure

Momentum

Knowing if it's a seasonally bullish month or a seasonally bearish month is a critically important part of your successful commodity trading game plan.

Seasonality is important, but how should we think about how seasonality works?

When commodity prices tend to rise during a certain time of the year, why is that?

Seasonals tend to generally follow production trends throughout a calendar year.

Traders tend to add what's called a ‘risk premium’ to futures prices during critical production months, and then price out that risk premium once production becomes more known.

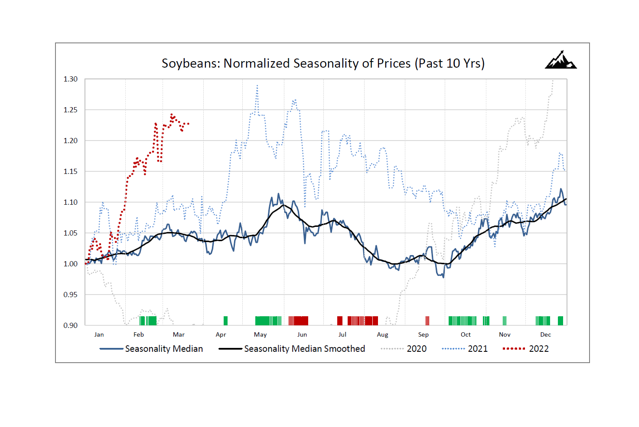

To take an example for a market like U.S. Soybeans, traders tend to get nervous in April and May as we're heading into critical summer production months for Soybeans.

But by the time we get to June and July and August, that window where things can really go wrong starts closing and traders start to remove that price risk premium that they had added in April and May.

Soybean futures prices tend to drop in late summer.

Every year is different and every year has a different mix of fundamental and non-fundamental price drivers that move prices, but if we take 10+ years of data we can get a sense for the big picture seasonal trends in futures prices throughout the calendar year.

At Peak Trading Research, we provide our clients with 10-year normalized price trends for every major commodity market (like we looked at for soybeans earlier).

We also provide our clients with heat maps to see the multi-week seasonal trends across the whole commodity complex.

And finally, we provide our clients with very specific high hit rate seasonal patterns every month.

For example, if we look at our March 2022 seasonal price patterns, we can see that Sugar No. 11 futures have dropped in 15 out of 17 years for the 27 trading sessions starting March 2nd.

That has been a consistently profitable bearish price trend in Sugar over the past 17 years.

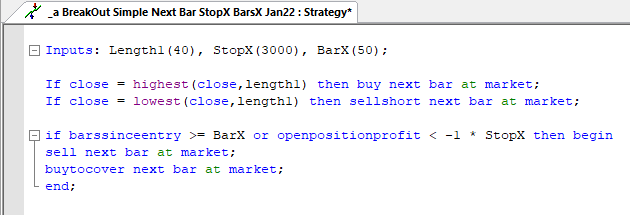

You can also analyze seasonal trends yourself using Excel or Python, or even an automated trading platform like MultiCharts or TradeStation.

For example, if you would use a simple script like this in TradeStation, you could test when the best time of the year is to enter a trade and also optimize to find how long you should stay in that trade.

We can see using that code that TradeStation is telling us what we already knew: that is selling in early March and covering that short in May is generally a profitable approach.

Seasonal code example:

Inputs: DayShift(0), BarsSince(84);

If date crosses over calcdate(1210228, Dayshift) then sellshort next bar at market;

If date crosses over calcdate(1200229, Dayshift) then sellshort next bar at market;

If date crosses over calcdate(1190228, Dayshift) then sellshort next bar at market;

If barssinceentry >= BarsSince then buytocover next bar market;

So, we've talked about the different ways that you can either use Peak Trading Research analysis or your own approach to find these seasonal trends, but what's the best way to trade seasonals?

How should you actually structure a trade?

Based on a lot of analysis and testing that we've run, the best way to structure a seasonal trade is to take whatever bullish or bearish move you expect to see based on your 10, 12, or 15 years of seasonal analysis - maybe it's a 5% move or a 10% move or a 15% move - and then take half of that as your stop loss.

So, if you're looking to make $5,000 on a short position in sugar, take $2,500 as your stop.

Now, a 2:1 risk-reward ratio may not seem that great. For example, if we were using a breakout strategy, we might use a 4:1 or a 5:1 risk-return ratio. But with seasonal trades, we really want to give the trade a wide berth. We want to give this trade a lot of room to work.

These are multi-week or multi-month trades. A lot of volatility can happen in the meantime before we finally realize that eventual seasonal pattern. From our experience, a 2:1 risk-reward ratio generally makes sense to think about structuring these trades.

Now, we've talked about examples for soybeans and sugar, but seasonals also work for energy markets, for metal markets, and interest rate markets.

To summarize:

Commodity markets have strong seasonal trends.

These trends exist because there are certain times when traders either add or remove a risk premium.

There are different ways to analyze those seasonal trends, either a big picture multi-week, multi-month view, or a more specific high hit rate window.

To structure a seasonal trade, something like a 2:1 risk-reward ratio tends to work best.

Thanks for reading and if you’d like a trial of our actionable commodity research - including our in-depth seasonal analysis - you can reach out for trial: Insight@PeakTradingResearch.com.

The Best Commodity Breakout Strategy - How to Trade Breakouts

Commodity markets are great breakout markets.

You can make a lot of money as a commodity trader by buying higher highs and selling lower lows.

Today, we’ll review the simplest breakout trading approach that works in many of the world's biggest commodity markets, like Crude Oil, Heating Oil, Gasoline, Gold, and Soybeans.

And we'll examine the results from 60,500 different tests to see what is the best agriculture market for breakout trading and what is the best energy market for breakout trading.

Breakout strategies work.

We're going to see in which markets they work best.

Let's get into it.

BUILDING A GREAT BREAKOUT STRATEGY

Today we're going to be building the simplest breakout strategy that we can test across a lot of different markets and bar sizes to prove definitively what are the best breakout markets.

We know that breakout trading is buying a higher high, or selling short a lower low, holding that position for some period of time, and hoping to make a profit.

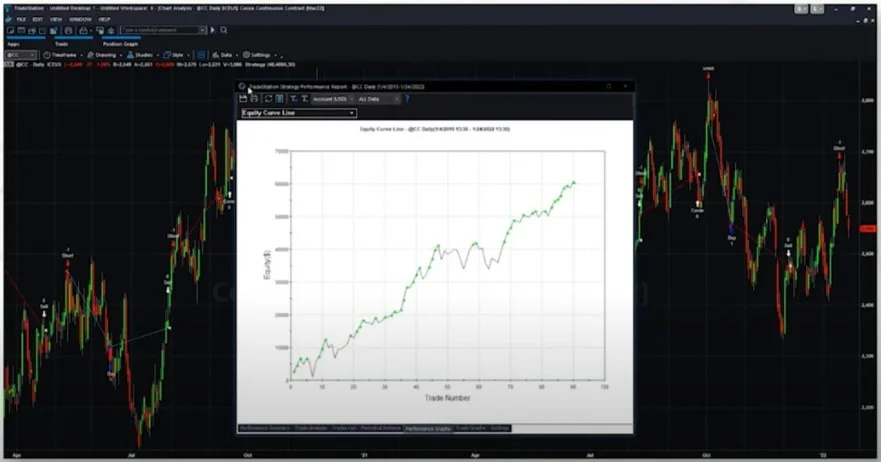

Let's start by jumping into some very simple EasyLanguage trading strategy code that illustrates how we're going to test this idea.

Simple Breakout Strategy Code

What is this complete trading system doing?

If the market closes at the highest level of the last 40 bars, the system will go long.

If the system closes at the lowest level of the last 40 bars, the system will go short.

Exits: if 50 bars have passed, or if the trade has lost more than $3,000 per contract, this system will exit the long or short trade.

This is a very simple but effective trading approach.

If the market goes up, you buy it.

If the market goes down, you sell it.

You get out after a certain amount of time and you've got a stop loss.

Simple stuff.

OPTIMIZATION

This is the fun part.

We can play around with those inputs in our strategy and test them across a lot of different markets and bar sizes to really tell us what are the best breakout markets. Our Algo Lab trading platform at PeakAlgo.com allows us to quickly test these different parameters.

We are going to test our length parameter from a value of 10 to 50. So if we were using daily bars in our chart, we'd be testing it from 10 to 50 days.

We're going to test a stoploss value from $1,000 to $5,000 per contract.

And we're going to test our exit bars also from a value of 10 days to 50 days.

So that's 5 (length) x 5 (stop) x 5 (exit bars) parameters = 125 different parameter combinations.

We're then going to test those parameter combinations across 44 different futures markets and 11 different bar sizes, e.g., 60 min bars, 180 min bars, 360 min bars, etc.

125 parameter combinations x 44 markets times x 11 bar sizes = 60,500 different tests.

Our Algo Lab platform tells us that there are nine different commodity markets in which our simple breakout trading system generates a significantly positive profit.

And that includes realistic slippage and commission costs.

Over the past 10 years, the best commodity markets for breakout trading are Crude Oil, Heating Oil, Gasoline, Soybeans, Soybean Meal, Lean Hogs, Gold, Palladium, and Silver.

THE BEST AGRICULTURE MARKET FOR BREAKOUT TRADING

The Lean Hogs market is one of the best agriculture markets for breakout trading.

The extremely simple breakout trading approach we tested on Lean Hog daily bars generates a pretty impressive cumulative equity line (below).

This tells us that if you're a professional commodity trader and you're trading Lean Hog futures, you should consider buying higher highs and selling lower lows.

Once Lean Hog futures start moving, they tend to keep moving. Our simple breakout trading strategy shows us that.

Profits: Breakout strategy equity curve (cumulative profit line) in the Lean Hogs market

THE BEST ENERGY MARKET FOR BREAKOUT TRADING

On the energy side, what is the #1 energy market for breakout trading?

The energy market that is responsible for this beautiful-looking cumulative equity line?

Heating Oil.

Equity curve in heating oil market running breakout strategy

Just to review, what have we done today?

We've built a simple breakout trading system.

We've tested the system across a lot of different markets and bar sizes (60,400 tests)

The results from our tests show us that some of the biggest and most well-known markets like Crude Oil, Gold, and Soybeans are great breakout markets.

Lean Hogs and Heating Oil are exception breakout markets.

Hopefully, this article helps you build, analyze, and trade breakout strategies across different agriculture, energy, and metal commodity markets.

For full access to our Algo Lab strategy testing tool, visit www.PeakAlgo.com and for our quantitative commodity research, visit www.PeakTradingResearch.com.

Mean Reverting Commodity Markets - Best Mean Reversion Strategy

We know that a lot of commodity markets are great breakout markets, i.e., markets where it makes sense to buy higher highs, and sell lower lows (see the full article here).

But what about mean reverting markets? i.e., commodity markets where it makes sense to sell higher highs and buy lower lows.

Now, there aren't many mean reverting markets in the commodity world, but today we're going to run 60,500 tests and find out which commodity markets are mean-reverting.

Let's get into it.

BUILDING AND TESTING A MEAN-REVERTING STRATEGY

Today, we're going to be building and testing a mean reversion strategy.

We're going to start with the same code from our breakout strategy article, and instead of buying higher highs and selling short lower lows, we are going to be selling short higher highs and buying lower lows.

This simple strategy is looking for markets that revert to the mean.

It's looking for markets that trade in a sideways channel.

Sample code for mean-reverting strategy

What is this complete trading system doing?

If the market closes at the highest level of the last 40 bars, the system will sell short.

If the system closes at the lowest level of the last 40 bars, the system will go long.

Exits: if 50 bars have passed, or if the trade has lost more than $3,000 per contract, this system will exit the long or short trade.

Again, this is a very simple trading approach.

If the market goes up, you sell it.

If the market goes down, you buy it.

You get out after a certain amount of time and you've got a stop loss.

Mean reversion. Simple stuff.

OPTIMIZATION TESTS

Using our Algo Lab tool at PeakAlgo.com, we can test those inputs in our strategy across a lot of different markets and bar sizes to really tell us what are the best mean-reverting markets.

We are going to test our length parameter from a value of 10 to 50. So if we were using daily bars in our chart, we'd be testing it from 10 to 50 days.

We're going to test a stop value from $1,000 to $5,000 per contract.

And we're going to test our exit bars also from a value of 10 days to 50 days.

So that's 5 (length) x 5 (stop) x 5 (exit) parameters = 125 different parameter combinations.

We're then going to test those 125 parameter combinations across 44 different futures markets and 11 different bar sizes, e.g., 60 min bars, 180 min bars, 360 min bars, etc.

125 parameter combinations x 44 markets times x 11 bar sizes = 60,500 different tests.

That's a total of 60,500 different tests that we're going to be running on this simple mean reversion strategy.

Algo Lab test parameters

TEST RESULTS - WHICH MARKETS ARE BEST?

After running 60,500 different tests on our simple mean reversion strategy, we can see that Nat Gas is a pretty good mean-reverting market. And Arabica Coffee works pretty well.

But there is one market that stands above them all as the king of mean reversion:

The Cocoa market.

If we look at a price chart of the Cocoa market, we can see that it exhibits some mean-reverting behavior.

It trades in a sideways pattern, where it generally makes sense to buy lower lows and sell higher highs.

Cocoa often trades in a sideways pattern and reverts to the mean.

And if we look at how this trading system has performed, we see a very nice, upward sloping equity curve (cumulative profit line), which means our simple mean reversion system has made money over time in the Cocoa market.

CONCLUSION

Although our simple mean reversion strategy doesn’t work in a lot of commodity markets, the good news is that our Algo Lab tool shows us that Cocoa is the world's #1 mean-reverting market.

If you're a professional Cocoa trader, you should really consider selling higher highs and buying lower lows. That is the trading approach that will make you the most money.

Hopefully, this article helps you build, analyze, and trade mean-reversion strategies across different agriculture, energy, and metal commodity markets.

For full access to our Algo Lab strategy testing tool, visit www.PeakAlgo.com and for our quantitative commodity research, visit www.PeakTradingResearch.com.

Why the U.S. Dollar Matters for Commodity Markets

If you're a professional commodity trader, you are very aware that macroeconomic inputs and macro money flows have a huge impact on the commodity markets that you trade.

One of the most important macro inputs is the U.S. dollar.

Why is that?

Why does the US dollar matter so much for all commodity markets?

In this article, we're going to go through the five reasons that the dollar matters so much for commodity markets. We'll also touch on the two ways that you can incorporate the dollar view into your profitable commodity trading. Let's jump into it.

THE U.S. DOLLAR MATTERS

Our goal at Peak Trading Research is to make you a more profitable trader with commodity market insights and real systematic trading strategies. A big part of profitable commodity trading is knowing how to incorporate macroeconomic inputs into your profitable commodity trading game plan.

And the U.S. dollar is one of the most important macroeconomic inputs to understand.

Let's talk about the five reasons why that is.

Yardstick Effect. The first and one of the most important reasons why the dollar matters so much for commodity markets is what we call ‘The Yardstick Effect.’ Most commodity markets are U.S. dollar-denominated, so if the U.S. dollar drops in value, prices of commodities rise as a function of the unit of measurement shrinking. That is, the yardstick shrinks. So if the value of the dollar drops, commodities are worth more dollars.

Macro Flows. The second reason why the dollar matters so much for commodity markets is because of macroeconomic trader flows. There are a lot of hedge funds that will use commodity futures as a way to express a macroeconomic view. These traders will often buy agriculture futures as a way to profit from the value of a falling U.S. dollar. This is sometimes referred to as ‘trading the U.S. dollar in the Wheat pit’, i.e., using commodities as the instrument of choice to express a view on the U.S. dollar.

Correlation Flows. The third reason that the dollar matters so much for commodity markets is because of correlation flows. There are a lot of systematic and high-frequency hedge funds that see the value of the dollar dropping and act quickly to buy commodity futures. These traders act really quickly - often in just a matter of seconds - to try and buy and sell commodities to front-run other fundamental flows. If these traders think the value of the U.S. dollar is going to drop, they are quickly buying commodity futures to profit from a rise in prices.

Fundamental Demand Response. The fourth reason that the US dollar matters so much for commodity markets is a fundamental reason: a fundamental demand response. Non-U.S. importers (countries and corporations outside of the U.S.) see a weak U.S. dollar as an opportunity to buy cheaper U.S. agriculture products.

One of the best examples of this is in Egypt. The government has set up a program called the General Authority for Supply Commodities, also known as GASC. Buyers at GASC are constantly looking around the world to see where they can source the lowest priced Wheat to bring home to feed the Egyptian population. So if the U.S. dollar is weak versus currencies in origins like Russia or Australia or Canada or Europe, naturally GASC will buy more U.S. dollar-denominated Wheat from the United States. If the dollar goes down, U.S. dollar-denominated Wheat goes up.

Fundamental Supply Response. The fifth and final reason that the U.S. dollar matters so much for commodity markets is another fundamental reason: a fundamental supply response.

For a good example of this, put yourself in the shoes of a Brazilian farmer or an Argentine farmer. If you see a weak U.S. dollar and a strong Brazilian real and a strong Argentine peso, you know that if you sell your Soybeans into the global market at a dollar price, you're not getting a whole lot translated back into your local currency.So if you see a weak US dollar, you're not going to export your Soybeans, you're going to put them in silos or put them in bags, you're going to sit back and reduce your exports. You're going to reduce the amount of supply in the market. And you’re also probably not going to plant as much. You're not going to expand your acres if you see a weak U.S. dollar and a weak global price for your Soybeans.

In summary, a weaker U.S. dollar means fewer South American exports and less South American acreage expansion, all of which leads to higher prices via reduced supply.

TRADING

To summarize, there are five reasons that the U.S. dollar matters for commodity markets: the yardstick effect, macroeconomic trader flows, correlation trader flows, fundamental demand response, and fundamental supply response.

We've established that the U.S. dollar matters for commodity markets for a lot of fundamental and non-fundamental reasons, but how can we make this actionable?

How can you take a U.S. dollar view and incorporate it into your profitable commodity trading game plan?

ORIGIN CURRENCIES AND DESTINATION CURRENCIES

The first way to do this is by understanding which currency markets are most important for the commodity market that you trade.

A lot of this has to do with looking at origins where the commodity is mined or grown and destinations where the commodity is imported.

For example, if you're a Soybean trader, you need to focus a lot on the Brazilian real or the Argentine peso where Soybeans are grown, and you also need to focus on the Chinese renminbi, because China is the world's largest Soybean importer.

Every commodity market is unique, but all follow that supply and demand framework, so you should think about origin currencies and destination currencies.

Key currencies to watch in the soybean market

CENTRAL BANK POLICIES AND ECONOMIC REGIMES

Another way that you can incorporate a dollar view directly into your trading is to analyze what kind of economic regime we're in.

For example, is U.S. data improving enough for the US Federal Reserve to start removing stimulus?

As the US Federal Reserve starts tapering its quantitative easing purchases and eventually starts raising interest rates, that will strengthen the U.S. dollar.

We last saw this in 2014. The last time the Fed was tapering their QE purchases, the US dollar rose and commodity prices fell.

BOTTOM LINE

Think about the currency pairs that matter most for your market.

Is it the Australian dollar or the Brazilian real or the Chinese renminbi?

And analyze the current economic regime, what central banks are doing, how data is performing, and how that might move the dollar over the months and quarters and years to come.

Hopefully, this article helps you understand the different ways in which the U.S. dollar impacts your commodity markets and how to use a U.S. dollar view to trade commodity futures more profitably.

If you're interested in live updates of the macroeconomic inputs that matter most for your commodity markets, you can reach out to us for a trial of our research: Insight@PeakTradingResearch.com.

Non-Commercial vs Managed Money Hedge Fund Traders

What's the difference between a non-commercial trader and a managed money trader?

At Peak Trading Research we get this question all the time.

If you're a professional agriculture trader, you know that hedge funds are the predominant price drivers in agriculture futures markets but maybe you're unclear on the differences between these two hedge fund categories.

Today, we're going to go through the differences between non-commercial and managed money traders and we’ll tell you which category we prefer for analysis and systematic trading.

Hedge funds are the dominant participants in agriculture markets.

We've talked about this in a previous article here. When hedge funds buy prices go up, when hedge funds sell prices go down. Understanding hedge fund positioning is important.

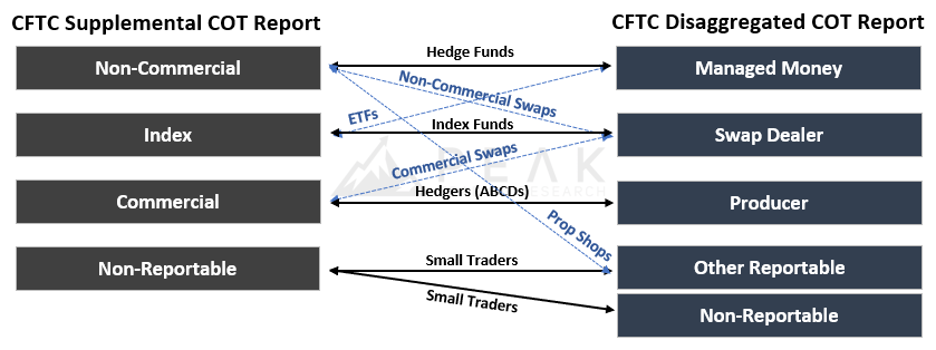

But the CFTC makes this a little confusing because they put out two different COT reports: a managed money position and a non-commercial position.

So what's the difference between a non-commercial trader and a managed money trader? And which one should you be looking at for your analysis and trading?

Before we jump into that, let's back up and look at all the categories within these two different reports.

Comparison of the 2 CFTC reports (Supplemental and Disaggregated)

If we look at the differences between the supplemental report and disaggregated report, one of the first things that jumps out to us is that the disaggregated report has an extra category.

All large speculators fall into the non-commercial report in the supplemental report, but large speculators are split up into two categories in the disaggregated report: managed money traders and other reportables.

This is the first reason that we prefer the non-commercial position to the managed money position. When you look at the non-commercial position, you have the confidence that you're looking at the position for all large speculators. When you look at managed money traders, you might be missing some important traders like family offices or Chinese speculators (other reportable traders). The non-commercial position quantifies the position for all large speculators.

The second reason that we prefer the non-commercial position to the managed money position is also just a function of our background and experience at Peak Trading Research. Dave Whitcomb, Head of Research, was an agriculture trader at Cargill for 12 years. Cargill is one of the world's largest commercial trading houses. It’s our experience that most commercial traders tend to reference the non-commercial position. Most hedge fund traders tend to reference the managed money position.

For example, if you were sitting in on a meeting at Cargill or ADM or Bunge, and you heard their head Corn trader say hedge funds are 200,000 contracts long Corn, it's very likely that that trader is referencing the non-commercial position *not* the managed money position.

So again, that second reason that we like the non-commercial position is that it's more often referenced by the world's largest commercial traders.

And finally, the third reason that we prefer the non-commercial position to the managed money position is that we prefer the supplemental report overall in the way that the categories are defined versus the disaggregated report. As we discussed earlier, the disaggregated report has two different categories for large speculators: managed money traders and other reportable traders.

And then there's the swap dealer category, which is just a mess. The swap category has non-commercial swaps, commercial swaps, and index swaps. It isn't as clean as the index category in the supplemental report. So, because we like the categories in the supplemental report more than the categories and the disaggregated report, it follows that we prefer the non-commercial position.

To review the three reasons why we prefer non-commercial versus managed money positions:

#1: The non-commercial position quantifies the positioning for *all* large speculators. The managed money category does not do that…it misses important ‘other reportable’ category traders.

#2: Large commercial trading houses like Cargill and ADM and Bunge usually reference the non-commercial position, not the managed money position.

#3: Categories are better defined in the supplemental report, which includes non-commercial traders.

Now, the one big advantage of the managed money position in the disaggregated report is that it covers more markets. If you're a trader in the Spring Wheat market or Oats or Canola or White Sugar or Robusta Coffee, you unfortunately only have a managed money position. You don't have a non-commercial position reported by the CFTC for your market.

Now, as we wrap up, there's one thing we want to emphasize, and that is if you're using the non-commercial position or the managed money position to build systematic trading strategies, you are doing the right thing.

You should not, for example, be trying to build trading systems around the index position or the commercial position or the garbage swap category. The non-commercial position and the managed money position are always the categories that will give you the best signals for your trading.

And as much as we've highlighted the differences between these two categories, they actually move in a very similar way. For example, if we look at the last 10 years, the correlation between the non-commercial position and managed money position in Corn is 0.90, in Wheat it's 0.92, in Soybeans it's 0.98! As much as we've highlighted a lot of differences between the non-commercial and managed money categories, they really do move together.

At Peak Trading Research we use machine learning to provide our clients with daily live estimates for non-commercial and managed money positions across all agriculture, energy, and metals markets.

If you'd like a trial of our research, you can reach out any time, insight@peaktradingresearch.com.

How to Build Profitable COT Trading Systems

Take a look at 3 systematic trading strategies in the Oats, Live Cattle and Kansas Wheat markets that have shown profitable equity curves. Learn about the basics of the code behind these systems so you can start making more profitable trades.

COT positioning reports can give you an edge and make you a better, more profitable trader.

Today, we're going to be going through three specific examples of profitable trading systems that you can trade, all of which incorporate COT positioning data.

This is the third article in a set of three.

In our first article, we talked about COT report 101. What is the report? Why does it matter?

In the second article, we talked about commodity market participants, with a focus on hedge funds.

And now in this third article, we're going to tie everything together.

This is the fun stuff.

We're going to be talking about how you can build real systematic trading strategies based on COT data, based on what we talked about in the first two articles.

Today, we're going to be going through specific trading systems for three different agriculture commodity markets:

Oats

Live Cattle

Kansas Wheat

All three of these trading systems use a pretty similar big picture idea:

Sometimes hedge funds get too long and sometimes hedge funds get too short.

We're going to be building systems that take advantage of either short squeezes or long liquidation events.

We’ll be going through these examples in TradeStation using TradeStation EasyLanguage, but if you're a discretionary trader, if you want to do this in Excel, or you want to build it in Python, that's no problem. We’ll use TradeStation so we can look at some basic profit statistics. But, most importantly, let's focus more on the logic of the systems and less on the specific code itself.

THRESHOLD TRADING

Now for this first trading system, we're going to be going through a very basic example of what we call COT threshold trading. We'll use Oats as an example. The questions we’ll be asking: Is the hedge fund net position above a certain threshold? Are hedge funds too long and vulnerable to a liquidation event?

We can build a very simple trading system using just two lines of logic that says whenever that non-commercial net position is above 2,200 contracts, i.e., when hedge funds are extended long, then we want to sell short Oat futures the next day on the market open. And after 21 days have gone by (about a month), we want to exit that short position.

Sample oat strategy with 2 lines of logic

Now, if we look at the strategy performance report, that's a nice upward sloping equity curve, meaning this strategy has generally made positive cumulative profits over time. We can see that it's made money in 12 out of 18 trades over the past few years.

This shows promise using a very simple approach that we could trade the Oats market using that non-commercial position as a threshold to establish shorts.

Equity curve line for sample Oat trading strategy

BIG FLOWS

Now for our second trading system example, we're going to be talking about big hedge fund flows.

Sometimes weekly COT reports show that hedge funds bought or sold a large number of contracts, and often that can send important forward-looking price signals about that market.

Let's look at an example for the Live Cattle market.

If we look at data from the August 24th, 2021 COT report, we can see that non-commercial hedge fund traders added 14,760 contracts of new longs during the week. That's the third-largest inflow week on record.

Now, if we look at the other 20 largest inflow weeks since 2006, we can see that Live Cattle prices generally drop during the one-month and three-month periods that follow.

live cattle market showing price changes after long inflows

Another way to say this is hedge funds tend to be “long and wrong” when they buy a lot of Cattle futures.

Hedge funds buy live cattle futures, prices go up, the market runs out of buyers, prices naturally settle back in the one- and three-month periods after.

We can see that happened in real-time. After we sent this note to clients on August 28th, 2021, if we look at what live cattle futures have done…they’ve settled lower, as predicted.

Live cattle market

THRESHOLD TRADING + PRICE SIGNAL

Now for our third and final trading system, we're going to be using the same threshold idea that we talked about in the first trading system, but also incorporating a price signal to trade.

Threshold trading is great. It's easy to understand, but it has one big shortcoming and that is hedge funds can stay extended long or extended short for long periods of time. It often takes some catalyst, some fundamental or non-fundamental trigger that moves prices against hedge fund positioning and drives all these funds to liquidate their big positions at the same time. We're going to build a trading system that uses this price trigger idea to trade profitably.

Now let's take the same code that we used in the first example for the Oats market, and let's apply it to Kansas Wheat. So in this case, if the non-commercial net position is above a 2,000-contract threshold, then sell short Kansas Wheat next bar at market.

kansas wheat sample strategy

We can see if we look at the strategy performance report, this is a decent trading approach - we've got a nice upward sloping equity curve.

This approach would've made $30,500 over the last 10 years using this approach. Not bad.

Kansas wheat equity curve

Now we can improve this a little bit.

We can also layer on a price signal.

Instead of only using a COT position threshold, we’re going to use a threshold PLUS a price signal of a two-day-low stop. So the system will sell short only if prices break through the lowest level of the past two trading sessions.

Kansas wheat sample strategy with price signal

Whenever momentum starts turning lower, this system is then going to sell instead of just selling above that threshold. Now, if we look at our strategy performance report, it's gotten a little bit better. Our P&L has improved.

Our profit line looks better. More profits, fewer drawdowns.

Kansas wheat equity curve with price signal

Now in both the Oats system in the first example and the Kansas Wheat system in the third example, we talked about selling short when hedge funds are extended long.

But there are, of course, other ways that you can trade COT data:

You could add more price filters to some of these systems or a seasonal filter or volume or momentum.

You could also incorporate positions from some of the other market participants we talked about in our second video: other reportables, non-reportables, commercial positioning.

There's a lot more you can do here.

If you are looking for more ideas on how to build trading systems around COT data, these are fantastic resources:

The Commitment of Traders Bible by Stephen Briese

Trade Stocks and Commodities with the Insiders by Larry Williams.

Hopefully this article gave you a good sense for how you can build profitable trading systems using COT data.

Any questions? insight@peaktradingresearch.com

COT Market Participants (Hedge Funds Matter!)

Today we're going to be talking about commodity market participants and why hedge funds matter so much for commodity markets. To get started, let's look at the big picture and talk about the four main participants in commodity markets.

That's hedge funds, index funds, commercial traders, and smaller private traders.

Hedge funds really matter for commodity markets.

When hedge funds buy, prices go up and when hedge funds sell prices, go down.

Today we'll talk about who these hedge funds are, how they trade, and how we can see the influence that these funds have on commodity markets in the weekly Commitment of Traders reports.

We'll also talk about some other important investor categories: index funds, commercial traders, small private traders, and how they all interact with one another to exert influence over commodity market prices.

To get started, let's look at the big picture and talk about the four main participants in commodity markets.

That's hedge funds, index funds, commercial traders, and smaller private traders.

HEDGE FUNDS

Let's start with hedge funds. You probably know what a hedge fund is. It's an investment fund that is trying to make money for its clients by speculating. For commodity futures, a hedge fund is trying to either buy or sell short commodity futures with the goal of making a profit for its clients.

Rhere are a lot of different hedge funds that use a lot of different information and price drivers to trade but broadly speaking, they fall into three main buckets:

Systematic traders

Fundamental traders

Macro traders

Systems traders are mostly using some combination of technical or momentum signals to trade.

Fundamental traders are using balance sheets, e.g., how much of a crop is grown, how much it's harvested, how much demand there is.

Macro traders are taking big-picture thematic views, for example, a view on the dollar or a view on inflation and expressing that via commodity futures.

There's been an important trend in the last 10 years and that is hedge funds are focusing more and more on non-nonfundamental trading inputs (momentum, seasonality, macro flows) and less on fundamental trading inputs (yields, production, demand).

Who are some of the big systematic hedge funds in commodity markets?

It's groups like Millennium, Winton, Two Sigma, Systematica, and Square Point.

And some of the fundamentally-biased hedge funds like Citadel or DE Shaw are using a ‘quantamentals’ approach to trade. They're blending quant style trading with fundamental inputs that they can backtest.

Now, how do we know that hedge funds have so much influence in commodity markets?

If we look at weekly CFTC Commitment of Trader report money flows, we can see that there's a positive correlation between the money that hedge funds are putting into or out of commodity markets and what prices do during the week. If hedge funds buy, prices go up. If hedge funds sell, prices go down.

Now let's take an example from a big liquid agriculture market like corn.

If we take the correlation between hedge fund flows and prices, we can see that they are strongly positively correlated. Meaning again, when hedge funds buy, prices go up.

We can see that mathematically, we can prove that out. And this is the same for most commodity markets.

Hedge funds are the price drivers for commodity markets.

POSITIVE CORRELATION SHOWING HEDGE FUNDS AS PRICE DRIVERS

In our third article on Commitment of Traders reports, we’ll talk more about building real systematic trading systems around COT data. We’ll give real examples of how we can use hedge fund positioning to inform profitable trading decisions in real-time.

INDEX FUNDS

Let's move on to index funds.

Index funds invest in commodities as a hedge against future inflation. They're using commodity futures as a store of value. Examples of index fund investors: pension funds, endowments, foundations, and sovereign wealth funds. These groups have a big pool of assets that they need to protect against the threat of inflation.

POPULAR COMMODITY INDEX FUNDS

These index investors will invest in a commodity index, a popular index like the Bloomberg Commodity Index or the Goldman Sachs Commodity Index, where the goal is to just hold a big bucket of commodities, e.g., crude oil, gold, copper, silver, corn, wheat, soybeans, cattle, and cocoa.

They just want exposure to the whole commodity asset class so that if prices start rising, they know that they have a hedge against inflation.

As you might have guessed, the number one trading input that index investors use when deciding to put money into or out of commodity markets is future inflation expectations.

If they think inflation's going to run hot over the near term, they're going to put more money into commodities as a hedge against future price rises.

What are some examples of index investors?

California Public Employee Retirement System

Harvard Endowment

Abu Dhabi Investment Authority

These are investors that are investing for multiple quarters or even multiple years.

They're long-term, slow-moving investors.

COMMERCIAL TRADING HOUSES

Now the third category is the commercial or producer category.

These are big commercial trading houses like the ABCDs: ADM, Bungee, Cargill, and Louis Dreyfus.

Commercial trading houses are generally price takers in commodity markets. Remember, we talked about hedge funds being the price drivers, commercial trading houses are usually the price takers.

Now, this does *not* mean that commercial traders are uninformed or slow. What it does mean is that they usually have cash positions against their future trades. These producers might view futures as expensive or cheap basis cash and they're more willing to take the other side of the trade that hedge funds have on.

If we look at the correlation between weekly producer and commercial flows and price changes, we can see this relationship: there's a strong negative correlation in a market like corn. When producers buy or sell, it doesn't have the same positive correlation as hedge funds.

Producers are the price takers.

Negative CORRELATION SHOWING index FUNDS AS PRICE takers

SMALL PRIVATE TRADERS

Now let's talk about this final category, the fourth category, that's small prop shops.

In the disaggregated COT report, there's this category called other reportables.

Other reportables are a mix of groups that trade a significant number of contracts but they're not managing money for other groups…they're managing their own money.

Other reportables are:

Option locals

Family offices

Chinese speculators

And finally, there are non-reportable traders.

Non-reportable traders hold a small enough position in commodity futures that they fall below the CFTC's reporting requirements.

Here is where you can find what exactly these limits are for each market (scroll to section 15.03):

The CFTC is trying to ensure the orderly functioning of markets. The CFTC doesn't want a few big players colluding to run markets up and down and squeeze everyone out.

If you’re a small trader and you hold five contracts of corn or ten contracts of crude oil, the CFTC isn't too worried about you running markets or causing any disruptions…they just don't need to hear from you so they put you in the non-reportable category.

To helps clarify things a bit, here are some of the differences between how investors are mapped between the two different COT reports (Disaggregated and Supplemental):

CFTC REPORT COMPARISON: SUPPLEMENTAL VS. DISAGGREGATED

Before you get too confused, remember to focus on the big picture:

Hedge funds are the price drivers in commodity markets.

Now for some markets, index funds can matter a little bit more or other reportable traders can matter a little bit more but by and large, keep in mind that hedge funds are the price drivers.

That is the group that you really need to focus on.

We'll come back to this idea a lot in our third article, where we talk about building real systematic trading systems around COT data and specifically around hedge fund position.

Peak Trading Research is the only research company that provides its clients with quarterly updates of correlations between price changes and weekly COT money flow so you can always see the evolution of which category matters most in your trading.

CORRELATIONS BY MARKET

As always, if you're interested in a trial of our actionable commodity research, you can reach out, insight@peaktradingresearch.com.

COT 101: What is the Weekly COT Report? Why Does It Matter for Profitable Commodity Trading?

Whether you are new to trading or an expert commodities trader, this video helps you understand and use the Commitment of Traders (COT) report in your daily analysis and trading. And most importantly, learn how to incorporate COT data into your systematic trading strategies.

Weekly Commitment of Traders (COT) reports are great. They can provide really valuable forward-looking information that can help you trade more profitably. Let’s talk about what the weekly Commitment of Traders report is, why it matters, and how it can make you a better trader.

To start: When are these COT reports published? They're published every Friday, with the exception of holidays. And, once in a while, there's a US Government shutdown - then the reports are delayed by a few days or weeks. Usually, they're reported every Friday.

But there’s a twist: COT data published on Friday is gathered as of the previous Tuesday. So the data is always delayed by at least three days. And by the time you get into the next week, that data becomes four, five, six, seven days delayed.

So, COT data is not published every day. It's not live. It’s always delayed by at least three days.

On the CFTC site (below), you'll find all the different COT reports listed by year. You can either use code, e.g., Python, to scrape the site, or you can simply download the reports as Excel (.csv) files for your analysis. A second option for finding COT data is to access it via a trading platform like Bloomberg or Reuters or TradeStation.

You can visit this site to view and download historical COT data.

CFTC website where you can access to the COT report each week

COT reports are especially valuable for agriculture futures - less so for energy or metal markets.

Why is that?

It's because most of the volume that's traded in agriculture markets is done via futures. The CFTC sees all that future's trading volume on its exchanges, and it says, "Okay, we can report that. We can quantify that and wrap our arms around that."

For energy and metals, there's a lot of trading volume that's done OTC (over the counter).

So COT data isn't quite as valuable for energy and metals as it is for agriculture markets.

Now without complicating things too much, there are actually two COT reports that you need to know about:

The Supplemental report: Agriculture specific. It has 13 agriculture markets.

The Disaggregated report: 150 different markets, including all major agriculture, energy, and metal markets.

The 13 agriculture markets covered in the COT Supplemental report

We'll do a deeper dive into the differences between the two COT reports and those market participants when we talk more about commodity market participants.

So what have we established?

The COT report is a weekly report.

It's always delayed by at least a few days.

It's pretty easy to find (website here).

It shows you positioning details across some important investor categories:

Hedge funds

Commercial traders

Index funds

Small private traders

Now, you might be saying, "Okay, that's great. How can I use this report to trade? How can I use the data that's in the COT report to make profitable trading decisions?"

You can find out more about building real systematic trading systems using COT data in the article here - but at a very high level, this is how you should think about trading COT data:

Imagine sitting down at a poker table and you can see most of your opponent’s cards. You can see what the other players hold. You don't know everything that they hold, but you have some very important clues about if they have a good hand or a bad hand.

That's how the CFTC COT report works.

You know that hedge funds are extended really long, or they're extended really short, or maybe index funds are extended really long, or they're extended really short, and you can see how vulnerable those positions are.

We're going to build some trading systems in our third article on COT reports around that idea.

Are hedge funds too long and vulnerable to a long liquidation?

Or are they too short and they're vulnerable to a short squeeze?

This COT information is tradeable. You can read more here.

Peak Trading Research is the only company that provides clients with daily estimates of COT hedge fund positions across all energy, metals, and agriculture markets.

If you're interested in a trial of our research, you can reach out to us at insight@peaktradingresearch.com.